Electric Vehicles, and the Perils of Too Much Investment

NBR Articles, published 14 December 2021

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall, originally appeared in the NBR on 14 December 2021.

One of the key ways in which equity markets serve both entrepreneurs and society is by facilitating the flow of capital into promising new ideas and technologies. If enough investors see promise in an early stage or rapidly growing business, it will be able to raise new capital from investors, and therefore achieve scale far earlier than would be possible if the business tried to fund its growth purely from internal resources.

Getting investors to buy-in to a company's prospects will be particularly important for those companies that have capital-intensive business models, as the need to fund capital investments will typically limit their ability to grow without outside investor capital. Companies may also want to use investor capital to turbo charge their growth trajectory if it is important to achieve critical mass before their targeted market attracts a lot of competition.

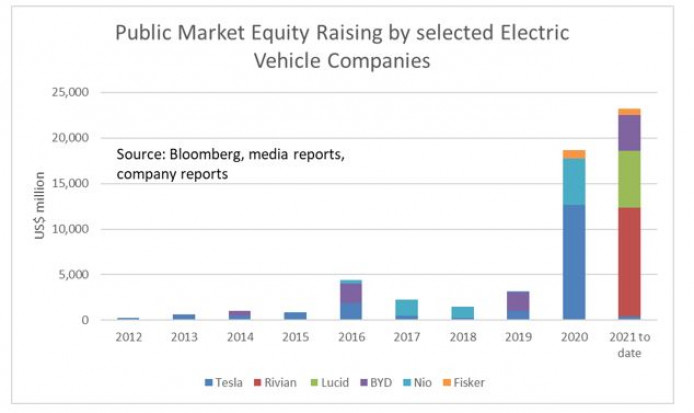

Electric vehicles are a classic example of this. Since Tesla listed on the sharemarket 11 years ago, it has raised close to US$25 billion in new equity, and has used this to build a strong position in the electric vehicle market, where it is the single largest manufacturer, with about a 15% share of the global electric vehicle market. Similarly, China's BYD has raised close to US$9 billion over the past decade, and used that to build a 6% share of the global electric vehicle market. Both companies are highly rated by investors, with Tesla now valued at over US$1 trillion (21.7 times annual sales), and BYD valued at US$127 billion (3.7 times annual sales).

Tesla's Gigafactory during construction

By contrast, many internal-combustion-focussed automotive manufacturers are valued by the market at less than one times annual sales. This includes companies like GM, Volkswagon, and Stellantis, each of which have more than a 6% share of global electric vehicle sales (greater than BYD's), but whose automotive manufacturing businesses are implicitly valued by the market at less than BYD's (and less than an eighth of Tesla's).

The share prices of Tesla and BYD have been particularly strong over the past 2 years, and they have taken advantage of this by raising more new funds from equity issuance than ever before.

In many ways, this is capitalism working like it's supposed to: investors thinking about the future have concluded that there will be strong demand for electric vehicles; they have purchased shares in companies like Tesla, which has led to high valuations for Tesla and other electric vehicle manufacturers; this is turn has meant that Tesla (and other electric vehicle manufacturers) have been able to raise more equity capital; and this will likely lead to an acceleration in the rate at which Tesla and other electric vehicle manufacturers can expand their electric vehicle production.

This all works very well for society as a whole, but how does the flood of capital affect the companies themselves? Until recently, Tesla seemed like a clear winner from the enthusiasm for electric vehicle investing (which it had pioneered). Strong investor appetite had meant that Tesla was able to raise the capital it required to expand its operations without having to incur significant dilution in the proportion of the company owned by pre-existing shareholders. And this expansion meant that Tesla was able to get a jump on the traditional (internal combustion focussed) car manufacturers, achieving a significant market presence before the established car manufacturers had a significant electric vehicle offering.

More recently, however, the attention that Tesla has grabbed for electric vehicles seems to have been working against it, by bolstering its competition.

For example:

- Electric Vehicle (EV) start-up Fisker listed in late 2020 and has since raised US$1.6 billion through issuance of new equity. Based on reporting up to the end of September, it does not appear to have sold any actual motor vehicles. The sharemarket is valuing Fisker at US$5 billion.

- EV start-up Lucid raised US$4.5 billion in an initial public offering in July, and is reportedly currently raising a further US$1.75 billion through the issuance of convertible notes. In contrast to its strong record of selling shares, Lucid had only sold US$0.0002 billion of vehicles up to the end of September 2021. The share market is valuing Lucid at US$62 billion.

- Another EV start-up Rivian had an initial public offering in November, raising US$11.9 billion. Rivian apparently only began selling electric vehicles in September. The share market is valuing Rivian at $102 billion, greater than the valuation of GM or Ford.

- Traditional automotive manufacturers like Volkswagon, General Motors, Ford, BMW, Stellantis (Peugeot, Citroën, Fiat, Chrysler), and Hyundai have noticed the share market’s enthusiasm for electric vehicles and responded accordingly. All of these companies are committing billions of dollars toward electric vehicle development and manufacturing and are planning to launch several new models of electric vehicles over the next few years. Many have publicly committed to be entirely electric within the next 20-25 years.

Eighteen months ago, there seemed to be a credible scenario that Tesla might maintain the electric vehicle lead that it had gained while the rest of the industry was napping, and that it might use this lead to build a 20%+ market share in an automotive market that would ultimately be exclusively electric. Bulls could extend this scenario to imagine that Tesla’s strong market position might enable it to achieve returns on invested capital that would be superior to the lacklustre returns on invested capital that the automotive industry has achieved for most of the last 100 years.

But the boom in the development of electric vehicles by both start-ups and established automotive companies makes it look increasingly likely that the future market for electric vehicles will be just as competitive as the market for internal combustion-based vehicles has always been. When you combine this competition with the capital intensity of automobile manufacturing and the price sensitivity that most consumers will have with respect to such a big-ticket purchase, the outlook seems to be for at best modest long term returns on invested capital. Regardless of how much market share you think Tesla will end up with, it becomes very difficult to justify Tesla’s trillion-dollar valuation if you accept that the returns they ultimately achieve will merely be a fair return on the capital they need to invest.

At a helicopter view, the balance between the demand and supply of capital is a key factor in determining the returns on invested capital achieved in any industry or sector. Too often, investors focus exclusively on the demand side of the equation and forget to think about the supply of new capital. This can be a dangerous mistake. For example, the airline industry achieved far stronger growth rates than the broader economy for decades up until covid, yet the average returns from airline businesses have generally been poor, as the entire sector has poured more and more money into buying new planes.

Further, there are no obvious “network effects” that could make electric vehicle manufacturing a “winner takes all” business, where going with the market leader brings clear benefits to consumers. It is possible that autonomous driving technology (which Tesla also do) could ultimately be a “winner takes all” technology, but Alphabet’s Waymo seems just as likely to win this race as any individual automotive company’s autonomous driving technology.

The share market’s enthusiasm for electric vehicles as an answer to climate change is also puzzling, in light of the relatively limited role they can play reducing carbon emissions without a major change in how electricity is generated around the world. In most countries, the marginal kilowatt hour of electricity is produced by burning coal, such that the short-term consequence of more electric vehicles being driven is that more coal will be burnt. If this is the consequence, then shifting to electric vehicles would make little difference to overall CO2 emissions. For example, I’ve calculated that my internal-combustion-based Toyota Corolla produces 530kg of CO2 per annum, but that the near-term consequence of switching to a Tesla Model 3 would be that Huntly’s output of CO2 would increase by 599kg per annum.

In the longer term, we would hope that that the increased demand for electricity could be met from increased renewable generation, but the increase in electricity demand from having a large proportion of the vehicle fleet shifting to electric could represent such a step change that it is likely to result in more coal being burnt over the next decade. This is particularly likely to be the case in densely populated countries where renewable opportunities are smaller relative to demand.

Hence, the bigger, arguably more difficult shift that the world has to make to prevent climate change is a shift away from fossil-fuel-based generation. New Zealand is fortunate in that the ratio of our land area to population means that we can credibly hope to achieve this on renewables alone, but in more densely populated parts of the world, it is difficult to see how this could be achieved without significant investment in nuclear-power-based generation, or a significant reduction in total electricity consumption. While electric vehicles are generating all the excitement right now, less sexy activities like nuclear and renewable energy generation will ultimately need to attract capital if the world is to significantly reduce its greenhouse gas emissions.

At a helicopter view, the balance between the demand and supply of capital is a key factor in determining the returns on invested capital achieved in any industry or sector. Too often, investors focus exclusively on the demand side of the equation and forget to think about the supply of new capital.