The Perils of Disproportionate Voting

NBR Articles, published 15 November 2022

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 15 November 2022.

If you were putting up the majority of the capital required to establish or fund a business, would you allow your business partner uncontestable control over the finances and direction of the business even though they had only put up a minority of the total capital?

Most clear-thinking people would avoid such a situation, even if they were partnering with someone they knew, trusted, and believed to have a stable mind. While many investors may be willing to fund someone else’s business and leave them with practical day-to-day control over how the business is run, they will invariably reserve the right to veto related party transactions and remuneration, and maintain some backstop right to force changes (in case their business partner goes completely off the rails).

Venture Capitalists have a range of contractual tools that allow them to either get their money back or to take control of companies in which they hold minority stakes if the founding entrepreneur fails to achieve agreed targets. In New Zealand, when companies list on the stock exchange, there is a generally a principle of one share = one vote, with a constitution that protects minority shareholders by requiring independent directors and setting a high voting threshold (75%) on some important issues.

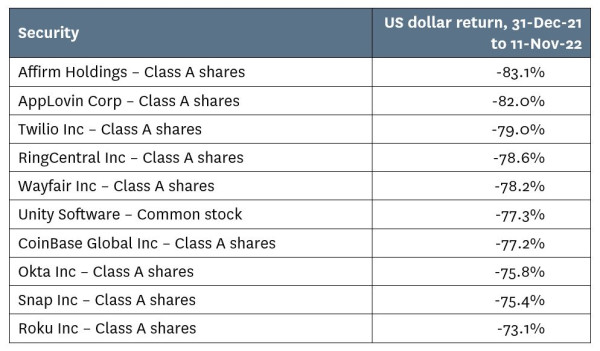

However these principles are not necessarily followed in other share markets around the world. To find some examples of this, let’s look at the ten worst performing stocks in the MSCI United States index so far this year:

Ten Worst Performing Companies in the MSCI United States Index

Notice something that 9 of these securities have in common? They’re “Class A shares”. In each case, these are listed shares that have diminished voting power compared to a class of unlisted shares that are held predominantly by the company’s founders or directors.

In each case, the “Class A” shares carry no more than one tenth of the voting power of the unlisted shares that are held by the company’s directors and founders. For seven of these companies, holders of the publicly listed shares have a majority economic interest in the company but control less than half of the total votes at a shareholder meeting.

Meta Platforms

If we look down beyond the worst 10 performing stocks, we find that many other poorly performing stocks also have diminished voting rights. For example, Meta Platforms’ Class A shares are the 15th worst performing stock in the MSCI United States index so far this year. Like the other Class A shares listed in the table above, Meta’s A shares carry diminished voting power compared to unlisted “B shares” that are held primarily by management interests (in this case, Mark Zuckerberg).

Meta Platform owns Facebook, Instagram, Messenger, and WhatsApp. These businesses have collectively generated US$47.8 billion of operating profits over the past 4 quarters and Meta holds US$15 billion of net cash. It seems reasonable to expect that if Meta Platforms only focused on these businesses and had a shareholding structure that allowed public shareholders to appoint directors who would act in their interests, it might carry a share market valuation of at least US$400 billion. However, a few days ago, Meta Platform’s market capitalisation fell to a low of US$235 billion.

Why was the market valuing Meta Platforms so much lower than the apparent value of its social media and messaging businesses? The key reason for this is that investors are concerned about the billions of dollars that Meta Platforms is pouring into its “Reality Labs” business. Reality Labs produces virtual reality headsets and has developed a virtual world called “Horizon Worlds” which Mark Zuckerberg thinks that people will want to use for business meetings in preference to either real life meetings or video conferences. In the latest quarter, Meta Platforms lost US$3.7 billion on the Reality Labs business, as spending on this business was 14 times as high as the revenues it produced. Meta’s guidance indicates that it intends to increase the amount of money it pours into Reality Labs over the next year.

Virtually everyone who isn’t Mark Zuckerberg thinks he’s delusional, and “Horizon Worlds” will never amount to much more than Second Life did in the first decade of this millennium. However, that probably won’t stop Meta from pushing ahead with Zuckerberg’s metaverse ambitions because although Mark Zuckerberg only owns 13.8% of Meta, he controls 58% of the votes at any shareholder meeting. This disproportionate voting power is because Zuckerberg owns over 90% of Meta’s “B shares”, which carry ten times the voting power of an “A share”.

If Meta Platforms had equal votes for all shares, the fire-sale pricing of Meta shares would almost certainly attract the interest of activist investors, whose game plan would be to build up a stake in Meta and then roll the board in favour of a new slate of directors who would stop funding the “Reality Labs” business. Such activist investors would hope and expect that these actions would lead to a restoration in Meta’s share market valuation. However, this scenario is not going to happen, because Meta’s unequal voting structure means that activists have no prospect of forcing any change.

One Share / One Vote still the norm in the United States

While my table showing the worst-performing companies could leave you with the impression that most companies listed in the United States have unequal voting structures, they are still very much in the minority if you look beyond the worst performers. For example, only 5 of the 100 best performing securities in the MSCI United States index this year are issued by companies that have unequal voting rights.

Other Countries

The United States is not the only country where many listed companies have different classes of shares with differential voting rights. Similar voting structures are common in Canada and Sweden, whilst many companies in Europe (particularly Germany) and Korea have issued preference shares that have identical (or superior) dividend rights to the ordinary shares, but lack any voting rights on most issues.

In most cases, both the ordinary and preference shares of these European and Korean companies are listed. In Korea, many of the non-voting preference shares trade at less than half the value of the voting ordinary shares, even though they have equal (or superior) dividend rights.

Outside of North America, these unequal voting structures are no longer in vogue, and appear to be hangovers from past fads for preference share issuance. If anything, the trend has been towards share class consolidation, with companies occasionally choosing to buy back preference shares or make proposals to convert them to ordinary shares. However, unequal voting rights in Europe sometimes mean that a founding family continues to control the board of a company by virtue of the unequal voting rights, and in the same way that turkeys don’t vote for Christmas, these founding families are unlikely to support any change to the status quo.

Why?

The reason that these unequal voting arrangements exist is essentially that founders put them in place when they were listing their companies. Most initial public offerings are launched in bull market environments, and investors queuing up for shares in these offerings will not quibble too much about a company’s voting arrangements if their quibbling might reduce the number of shares they are allocated in the IPO.

It is easy to understand why people listing their companies may want to retain super-voting rights. Many owners of private businesses shudder at the thought of having to answer to pimply-faced broker analysts demanding change because quarterly earnings were lower than expected. These private business owners have often grown their businesses by investing in new areas that generated losses for several years before turning to profit. They fear that the (sometimes) short-term focus of listed equity markets could make it impossible for them to expand their business in new areas. Establishing a voting structure that locks in their control is one way of addressing these fears.

But for public market investors, these unequal structures have the potential to become a real burden if the controlling shareholders dabble in areas where there is a conflict of interest, embrace wacky ideas (see Meta discussion above), or simply cease to be interested in the business (as is arguably sometimes the case when the descendants of a company’s founder end up inheriting the shares). Such circumstances will often add credence to Winston Churchill’s remark that “Democracy is the worst form of Govern[ance] - except for all the others that have been tried”.

While it is easy to disregard unequal voting structures when things are going well, public market investors ought to be a little wary of investing in such structures. Avoiding these structures altogether would probably be going too far, as there are plenty of examples of companies that have delivered good results for shareholders despite an unequal voting structure.

Many family-controlled European business with unequal voting rights have delivered good long-term returns, and Alphabet has also achieved strong long-term performance for shareholders, even though most of its votes are controlled by the Class B shares that only hold a 6.8% economic interest in Alphabet. It probably helps that no individual holds more than 45% of Alphabet’s class B shares, such that Alphabet’s public shareholders can assume that even if one of Alphabet’s 3 key founders (Larry Page, Sergey Brin, and Eric Schmidt) goes crazy and wants to pour billions of dollars into something like the metaverse, the other founders would be able to out-vote them.

Nicholas Bagnall is Chief Investment Officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios invest in companies discussed in this article, including Alphabet and (regretfully) Meta Platforms.