What if China invades Taiwan?

NBR Articles, published 28 June 2022

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall, originally appeared in the NBR on 28 June 2022.

The economies of both Mainland China and Taiwan are crucially inter-linked with the rest of the world. However, a sword of Damocles hangs over these critical components of the world economy, as mainland China continues to claim that Taiwan is part of China.

China’s claim is grounded in the fact that Taiwan was controlled from mainland China for a total of 216 out of the 6,500 years that it has been occupied by humans. From 1945 up until the 1990s, China’s claim was arguably better justified than it is today, as Taiwan was then controlled by authoritarian Chinese nationalist soldiers who relocated to there in 1949 after losing a civil war to the Chinese Communist Party. In some respects, the authoritarian government of Taiwan over that period was just as repressive as the communist rulers of mainland China.

However, in the last 30 years, Taiwan has evolved into a modern liberal democracy run and populated by people who were born in Taiwan who have always known it as an independent state. As a consequence, China’s claim over Taiwan has become increasingly divorced from reality, and democratic governments of the world would likely feel compelled to defend or at least assist Taiwan if China tried to take it by force.

But at the same time, the Chinese Communist Party’s willingness to push boundaries with the rest of the world seems to have only increased under Xi Jinping. There is clearly some risk that China could attempt to invade Taiwan at some point in the next decade.

Implications

A Chinese invasion (or attempted invasion) of Taiwan would have massive consequences for the world economy, likely causing disruptions that would be orders of magnitude greater than the impacts we have seen from Russia’s attempted invasion of Ukraine.

As a fund manager who believes in paying particular attention to downside risks, this is a risk that I need to pay particular attention to, as it has the potential to cause a severe decline in equity markets.

Russia/Ukraine presents a worrying precedent:

- Russian securities became virtually worthless overnight;

- Western companies with Russian operations have been forced to give them up for virtually no compensation; and

- many other companies have been affected by supply chain disruptions caused by both the Ukrainian war and the sanctions on trade with Russia.

But Russia was small bear compared to China. Many of the developed world’s largest companies get a large proportion of their revenues and profits from Greater China, or are critically dependent on Taiwan or China for their supply chains.

Mainland China’s exports to the rest of the world are about 7 times as large as Russia’s were, and it dominates global production in a lot of components. Even Taiwan (with a land area smaller than Canterbury) is a bigger exporter than Russia was, and it dominates global production of high-spec semiconductors. Most companies producing any form of electronics would have to cease or significantly reduce production if components from China and Taiwan became unavailable.

How should we think about this from an investment perspective?

Although I’ll freely admit to being no geo-political expert, it seems to me that a reasonable estimate of the probability of China trying to invade Taiwan at some point over the next decade is something in the order of 20%. Annualised, this works out at a probability of about 2% per annum.

If we use Russia’s invasion of Ukraine as a precedent for the likely consequences, that seems like a 2% per annum probability that investors could lose pretty much the entire value of any investment they hold in Chinese companies.

This 2% probability of complete loss should be a huge detractor from the investment case for any investment in a Chinese company. For example, in order for a Chinese stock to promise an expected return* of 8% per annum after factoring in the 2% risk of complete loss, we would need to expect it to deliver a 10.2% per annum return in the absence of an attempted invasion of Taiwan.

* Note: In this column I use the term “expected return” in the same way that is used in finance theory, meaning the weighted average of all possibilities. For example, an expected return of 8.00% is calculated as a 98% chance of a 10.2% return plus a 2% chance of a -100% return.

However, a 2.2% increment to the investors’ expected return in the absence of an attempted invasion would be insufficient to compensate for the risk. Investors need compensation for risk that goes beyond restoring expected return. Most people are intrinsically risk averse and get more value from certainty of having $108,000 in a years’ time than the 98% probability of having $110,205. This is why we buy insurance even when we expect the insurance company to profit from our business.

In investing, the need to be compensated for risk applies particularly strongly to risks that are difficult to diversify away from. It would be very hard to diversify an equity portfolio aways from the risks associated with a Chinese attack on Taiwan, because so many companies around the world would be affected by it.

To compensate for the extra risk that Chinese-exposed companies potentially bring to a portfolio, I would argue that expected returns need to be at least 0.5% per annum higher. Hence, we should demand at least an 8.5% per annum expected return from a Chinese company with characteristics for which might only call for an 8% expected return if the company were based in a less risky country. In order to anticipate an expected return of 8.5% per annum after factoring in the risk of China attacking Taiwan, we would need to expect a stock to deliver a return of 10.7% per annum in the absence-of-invasion.

What does this mean for stock prices?

If we could reliably assume that the risk of China invading Taiwan would completely disappear after ten years, stock prices would (based on the logic made up to this point in the article) need to be discounted (relative to where they might otherwise trade) by between 16% and 22% to compensate for the risk of an attempted invasion.

But if we assume that this risk could continue to be present for several decades, then an argument could be made that the level of discount required on Chinese stocks should be between 25% and 50%. The lower level of discounting would apply to those companies where most of the expected return comes from dividends (because, for example, if the invasion occurs in 10 years’ time, then you could have already got most of your initial investment back in the form of dividends), whereas a higher level of discounting would be required for Chinese companies where most of the expected future return comes from growth.

An argument can certainly be made that many listed Chinese companies are already heavily discounted by the market (trading at much lower multiples than comparable companies in the rest of the world). For example, the share market values China Tower, which owns 2,045,000 cell phone towers in China, at an enterprise value of US$36.2 billion, whereas it values American Tower, which owns just 221,000 cell phone towers around the world, at an enterprise value of US$176 billion (which works out at about US$160 billion for the cell phone towers once we strip out the value of some data centres that American Tower owns). At an extreme, you could use “value per cell phone tower” to argue that China Tower is trading at a 97% discount to American Tower, and that it’s valuation discount more than fully compensates for the risk of China doing something silly with Taiwan.

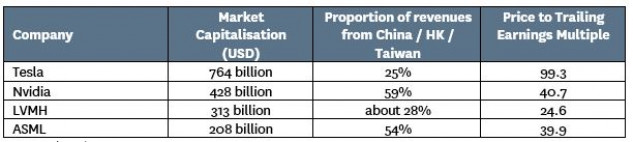

However, this discounting is not always so apparent when you look at western companies that do significant business in China. In the table below I give a few examples of western companies that are valued on high valuation multiples despite getting a significant share of revenues from China (including Hong Kong) and Taiwan.

Source: Bloomberg & Company Reports

It is not at all apparent that the share prices of any of these companies are pricing in anything for the risk of China invading Taiwan. Investors in these companies should be aware of their exposure to China, and make sure that they are taking account of it when evaluating their investments.

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios hold shares in China Tower.