America’s Zombie Banks

NBR Articles, published 28 March 2023

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 28 March 2023.

Many reports on the recent collapses of Silicon Valley Bank, Signature Bank of New York, and Credit Suisse have attributed these collapses mainly to sudden withdrawals of funds by depositors. While the runs on these banks were undoubtedly the first-order cause of these collapses, the emphasis on this aspect of the banking collapses obscures the fact that Silicon Valley had a more serious issue well before the run on its funds began – namely that that the value of its assets had already fallen below the value of its liabilities by the end of 2022.

How Silicon Valley Bank Lost So Much Money

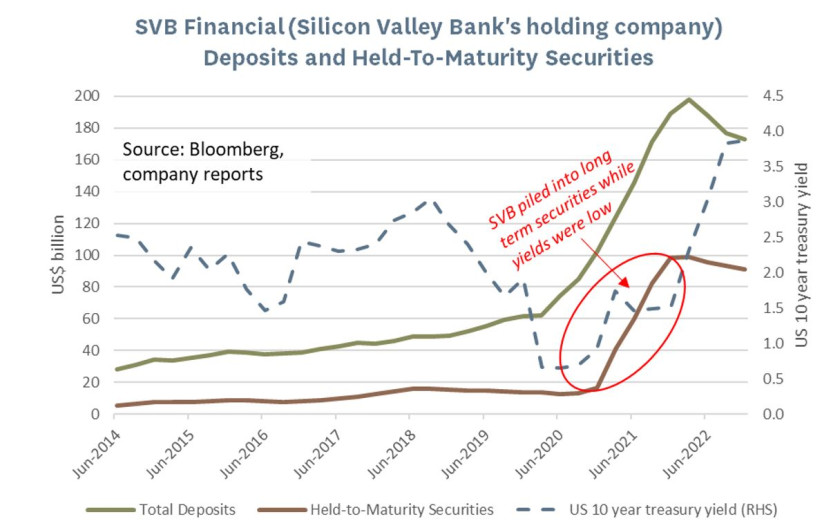

Silicon Valley Bank had wiped out its entire equity capital through a catastrophic failure in interest rate risk management. As it took on large amounts of on-demand, overnight, and other short-term deposits from depositors over the course of 2020 and 2021, it had invested a large proportion of the funds it received in long-term fixed interest securities. As these securities bore a fixed rate of interest, they stood to decline in value if market interest rates rose.

Silicon Valley Bank (“SVB”) was not merely investing in securities with one or two years of remaining life (which would only fall modestly in value as interest rates rose). Instead, 94% of the fixed interest investments that SVB classified as being “held to maturity” in December 2022 had contractual maturity dates of more than 10 years into the future. The bulk of these securities were invested in mortgage backed securities backed by 30-year fixed rate mortgages, where the underlying home borrowers typically had the right to pay off their mortgage early without penalty (as is normal in the United States).

If interest rates had stayed low, historical experience would suggest that the average life of these securities would prove to be much shorter than the contractual term. However, as we know, interest rates have risen significantly since the end of 2021, which means that many of the underlying mortgage borrowers have locked in very cheap funding, which they will probably now hold onto for as long as they possibly can. Even if they have the cash available to pay off their mortgages, the average US homeowner who took out a 30 year mortgage against their house in 2021 can now get a better return by buying US government bonds than they would achieve by paying off their mortgages.

The flip side of borrowers holding onto their cheap funding will be that SVB was effectively locked into getting a poor return on its long-term mortgage backed securities for a very long period of time, and as a result the market value of these securities had fallen to 17% below the value recorded on SVB’s balance sheet by the end of 2022.

The harsh reality is that the unrealised losses on SVB’s “held to maturity” fixed interest securities had wiped out all of SVB’s ordinary shareholders’ equity by the end of 2022. While the scale of the unrealised losses was disclosed in the notes to SVB’s accounts, it was not directly shown in SVB’s balance sheet, as a peculiarity of US accounting rules means that if US banks classify fixed interest securities as “held to maturity”, then they can show them on their balance sheet at amortised cost, regardless of how far this may be from the reality of market pricing.

The recent US practice of valuing a large proportion of fixed interest securities at amortised cost differs from the normal practice for banks in other countries, which typically record the vast majority (if not all) of their marketable securities on their balance sheet at market value. One factor behind the unusual US accounting could be that US banks prepare their financial statements according to US Generally Accepted Accounting Practices (US GAAP), whereas banks in the rest of the world use International Financial Reporting Standards (IFRS). However, both accounting standards give companies some discretion to choose to value some securities at amortised cost, so the real explanation as to why US banks use cost-based valuations for a large proportion of their fixed interest securities may be more to do with US banking culture.

Old school accountants sometimes like to argue that unrealised market gains and losses aren’t “real”. I reject this viewpoint. SVB’s market value losses are very real from two perspectives: firstly, declining market values meant that if depositors wanted their money back, SVB could no longer meet these demands by selling securities; and secondly even if depositors had continued to leave their money with SVB, its woeful interest rate risk management would have severely impacted its profitability over the next decade (as discussed in the paragraph below).

SVB had borrowed short term money and invested it in long-term securities, presumably accepting this duration mismatch because investing for longer terms allowed it to get a slightly higher yield and therefore report a higher net interest margin to equity investors who sometimes focus too much on short-term profitability. By accepting such a mismatch between the duration of its assets and liabilities, SVB exposed itself to the risk of a rise in funding costs. Since the end of 2021, short-term US interest rates have risen from 0.25% to 5.0%, which means that even if SVB was perceived as having rock-solid credit quality, depositors would now be requiring a much higher interest rate on their deposits. SVB had invested almost $1oo billion of the funds it received from short term deposits in long-term “held-to-maturity” securities, which means that if it had to pay 4% more per annum to hold onto these funds, it would now be facing an increase in funding costs of $4 billion per year without any corresponding increase in the interest income that it could expect from its held-to-maturity security portfolio. Given that SVB only had $17 billion of shareholders’ equity, the inevitable $4 billion per annum deterioration in its net interest income was probably destined to wipe out the shareholders’ equity that it records on its balance sheet within a few years (even if depositors had been prepared to overlook the fact that it had lost all its money on a marked-to-market basis).

Other US banks are doing it as well

Silicon Valley Bank is not the only US bank to have stashed funds from short-term deposits into long term investments.

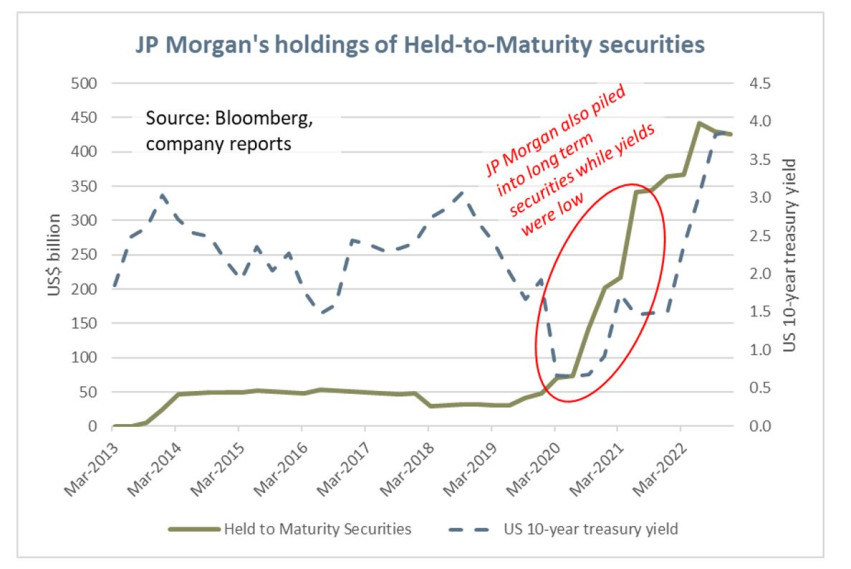

Given (1) US accounting rules that don’t require them to revalue held-to-maturity securities and (2) the tendency of US companies to focus on producing quarterly results that will appease share market investors, the majority of US banks seem to have fallen victim to the temptation of yield pick-up and bought large quantities of long duration investment securities over 2020 and 2021. For example, the graph below shows that just like Silicon Valley Bank, JP Morgan ploughed a lot of money into held-to-maturity fixed interest securities while yields were historically low in 2020 and 2021. In fact, the 665% increase in JP Morgan’s held-to-maturity fixed interest securities over 2020 and 2021 exceeds the 609% increase in SVB’s held-to-maturity securities. The saving grace for JP Morgan is that the dollar increase in its exposure was comparably smaller in relation to its equity capitalisation.

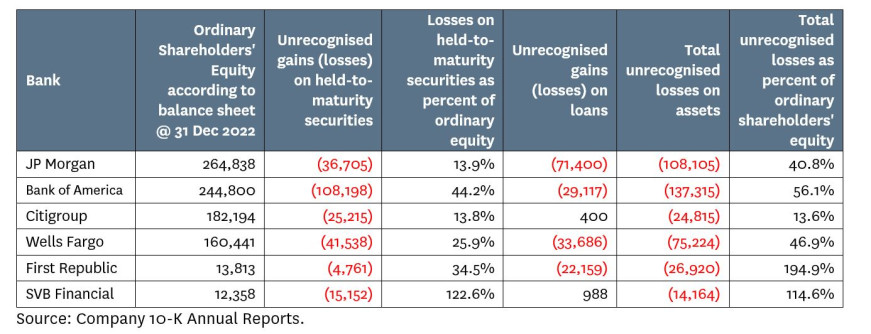

As a consequence of the US banks having poured so much money into long term fixed interest securities, most of them are now facing significant unrecognised losses on their held-to-maturity securities. The third column in the table below shows the unrecognised losses that select US banks have made on held-to-maturity securities (up to 31 December 2022), and the fourth column shows what these losses represent as a percentage of ordinary shareholders’ equity. In this table, I show data for the 4 largest US banks, as well as SVB Financial (the holding company of Silicon Valley Bank) and First Republic Bank (which is currently facing a lot of pressure from depositor withdrawals).

As can be seen from column 4 of the table, SVB was clearly the worst offender at piling funds from short term deposits into long-term securities, but many other banks also face significant unrecognised losses because they have similarly ignored interest rate risk to chase higher yields. Notably, Bank of America, the second largest US bank, faces unrecognised losses on its held-to-maturity securities that would wipe out over 44% of its ordinary shareholders’ equity.

You will not see such large unrecognised losses in banks in other parts of the world, because these banks record the vast majority of their security holdings at market value, and therefore generally manage their marked-to-market interest rate exposure to ensure that it will not have a significant impact on their reported equity. Also, most central banks outside of the United States insist that banks keep a tight rein on their net interest rate exposure, whereas the US Federal Reserve seems to have left US banks to their own devices.

Most banks outside of the United States hold the majority of their fixed interest securities in securities with less than 3 years remaining to maturity. The value of these shorter duration securities is less sensitive to rises in interest rates.

Long duration loans

Holding large quantities of long duration fixed interest securities seems particularly absurd in the case of US banks, as many American banks have long duration asset books even before taking account of their securities portfolios. The fair value of their lending books is very sensitive to interest rates due to the fact to that the standard product in the US home mortgage market is a 30-year fixed rate mortgage. Even without holding any securities, US banks are far more vulnerable to rises in interest rates than banks in other parts of the world.

The fifth column in the table above shows the losses (or in some cases, small gains) that the various US banks would face if their loan books were marked to market. The sixth column adds this to the unrecognised losses on fixed interest securities, and the seventh column shows the combined loss as a percentage of ordinary shareholders’ equity. On this metric, First Republic Bank appears to be even more insolvent than Silicon Valley Bank, and three of the big four US banks have lost more than 40% of their shareholders’ equity.

Valuing loans at amortised cost is normal in all jurisdictions, not just the United States. As a consequence, a few non-US banks that have significant exposure to fixed rate lending will also be sitting on significant unrecognised losses. For example, the fair value of Deutsche Bank’s loan portfolio is €22.6 billion lower than its carrying value, a shortfall that amounts to 37% of Deutsche Bank’s ordinary equity. Similar to the United States, the German mortgage market is based around long-term fixed rate mortgages, which become less valuable to banks when interest rates rise.

Diligently following the vacuous mantra of “best practice risk management”, many US banks appear to have got comfort from seeing that most of their peers were managing interest rate exposures in the same way as themselves, rather than independently thinking about how they would be affected by a rise in interest rates.

Why were American banks taking so much risk?

It seems to be an unwavering rule of competitive markets that if participants are measured on short-term performance, yet don’t perceive that their stakeholders are paying much attention to risk, then a large proportion of them will take on more and more risk in pursuit of short-term performance. The inevitable consequence of many participants accepting more risk in the hope of better returns is that they shift market pricing up to the point that they’re not really getting any incremental return in consideration for all the additional risk that they’re incurring. This pattern certainly seems to prevail in equity markets, where higher risk stocks have delivered worse returns than the rest of the market over long periods of time, and I suspect it’s also the case in banking.

If you look through the numerous historical instances of bank collapses or near-failures, a common element seems to be that the banks that have failed are those that have most enthusiastically plunged into whatever form of banking business seemed to be generating the best returns. We’ve seen this in New Zealand with Bank of Scotland International’s lending to all the property developers who subsequently went bust in 2008, and in BNZ’s lending to all the investment companies in the mid-1980s. In the United States, many of the banks with high levels of exposure to sub-prime lending failed or required significant recapitalisation during the GFC. Signature Bank of New York’s recent failure also seems to fit the pattern (even though it did not have as much interest rate exposure as many US banks), as it had prioritised profitability ahead of risk in its embrace of all things crypto.

The US banks’ huge duration mismatch was just another example of prioritising short-term performance ahead of risk. If JP Morgan (for example) had not bought US$400 billion of long-term fixed interest securities over 2020 and 2021, and had instead just invested the money it received from depositors in short-term treasury bills, the consequence could have been that it would have “missed out” on something like US$5 billion of pre-tax income in 2021. Rather than taking this more conservative approach, it seems to have prioritised short-term profitability, and is consequentially now facing a far bigger unrecognised loss on the value of the long term fixed interest securities that it purchased. As the table showed, the situation is even worse at other banks.

Zombie Banks

Modern economies depend on their banks. If banks are either unwilling or unable to lend (“zombie banks”), an economy inevitably heads backwards.

The recent collapse of Silicon Valley Bank highlights a failure of risk management that is prevalent across the majority of American banks. Many American banks have lost a large proportion of their equity capital, which is likely to limit their willingness and ability to lend. The jitteriness created by recent bank runs will further reduce the willingness of banks to lend money. A halt in new lending will likely lead to a period of low or zero growth in the US economy.

There are many precedents for this scenario. When I first began working in financial markets in the late 1980s, the United States was still reeling from the “Savings and Loan crisis”, whereby US regional Banks (then known as “Savings and Loan banks”) had made almost exactly the same mistake that they subsequently repeated in 2020 and 2021, taking short term deposits and investing the proceeds in long-term fixed-rate loans, only to be caught out by the high interest rates caused by Volcker’s attempt to rein in inflation in the early 1980s. The reduced ability of banks to lend led to a period of sub-par US economic growth, as many US banks were effectively zombies, kept “alive” by bail-out measures, but not really having sufficient equity to expand their lending.

During the US Savings & Loan crisis, Japan was perceived as the world’s most dynamic economy (similar to how the United States has been perceived in recent years), and by 1989 the four most valuable companies in the world (by market capitalisation) were all Japanese banks. But this all ended in 1990 after a collapse in the Japanese property and equity markets saddled the Japanese banks with a massive volume of non-performing loans. For almost two decades after this collapse, the Japanese banks were effectively “walking dead”, probably insolvent if they had taken appropriate provisions against their non-performing loans. Over this period, new loan origination ground to a halt in Japan, and the previously top-performing Japanese economy has stagnated ever since.

During the Global Financial Crisis in 2008 we got another brief taste of what it can be like when a banking sector is facing big potential losses and is therefore seeking to preserve cash. Corporate borrowers all over the world struggled to roll over maturing debt, and the lack of available debt finance caused several fire sales and receiverships over a short period of time.

It is now America’s turn all over again. As we saw in the table, a large number of big US banks have wiped out a significant portion of their equity. With less equity to back their lending, these banks will need to scale back their lending over the next few years.

Although the jitteriness of depositors has not been limited to the United States (Credit Suisse collapsed in Switzerland, and markets are currently running scared on Deutsche Bank), the wipe-out of equity due to poor interest rate risk management appears to be a problem that is mainly confined to US banks. I would therefore expect that the banking crisis may be relatively short-lived in most parts of the world, but that problems with US banking may take as long as a decade to unwind. If this proves to be the case, the failure of Silicon Valley Bank may signal an end to America’s period of superior economic growth.

Nicholas Bagnall is Chief Investment Officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios include holdings of Citigroup, and several non-US banks.