Pricing for growth or maximising profit?

NBR Articles, published 3 March 2026

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 3 March 2026.

Many businesses have a fair degree of discretion in how they price their products or services.

The decisions they make on pricing will involve a trade-off between profitability and growth. For businesses with reasonably sticky customers, higher pricing will typically lead to at least a short-term improvement in profitability, but this will normally come at the expense of longer-term growth.

In the graph below, I schematically show this relationship. On the left of the graph, we have a strategy of lower pricing, which will tend to boost growth by attracting new customers, but (obviously) lower prices mean that the company earns less profit from each customer. As we move to the right, higher prices lead to higher profitability per customer, but could potentially lead to the loss of customers over time.

As investors, we often use current profitability as a starting point for valuing companies. But the multiple we should pay for those earnings depends on how sustainable they are, and what prospect there is of earnings growing (or shrinking) from the current level. To assess this, it can be important to get a sense of whether the company is setting high prices (to boost profits) or setting very low/competitive prices (to fuel and protect future growth).

If a company is charging its customers very high prices, then there is a likelihood that it may either lose customers or be forced to cut its profit margins in the future. Paypal and Lululemon are examples of companies that were arguably “pushing the envelope” in how much they charged customers and have consequently seen slowing growth and a marked decline in their share prices over the past year.

I would have also added Adobe to this list if it weren’t for the inconvenient fact that, despite all the complaints I hear about what it charges for its software, its revenue growth has not really slowed down (yet). Nonetheless, it seems to me that Adobe is more at risk of losing customers to future competition when it charges customers up to $131 per month for a software suite (Creative Cloud Pro) that many users only use for a few hours a month. This seems like an aggressive approach when compared to the pricing strategy of Microsoft, which charges up to $36 per month for software that many of its customers are using almost continually.

In contrast to the “price gougers”, other companies aim to keep their prices low to boost growth. This means that the annual profits of these companies will often be a lot lower than their intrinsic potential. But you don’t need to feel sorry for the shareholders of these companies, as in exchange for the sacrifice of short-term profits, they will typically enjoy the growth benefit of more and more people choosing to become customers of the company.

Costco’s incredible growth over the past 3 decades (15-fold growth in sales, a compound growth rate of 9.5% per annum) can largely be attributed to its practice of keeping mark-ups very low and passing cost savings on to customers. Costco only take a gross profit of less than 13% of sales, but with high turnover and low operating costs, it nonetheless manages to achieve returns on equity of over 30%.

Foreign exchange payments company Wise is following a similar playbook, by proactively reducing the foreign exchange margins that it takes from customers as improving economies of scale lower its costs-per-transaction. Wise’s approach of progressively reducing its already-competitive foreign exchange take-rates has contributed to 36% per annum growth in customer numbers, 25% per annum growth in foreign exchange volumes, and 41% per annum growth in customer balances over the past 4 years. As a happy customer of Wise, I can report that I have not needed all these price cuts to keep me choosing it ahead of international bank transfers or the foreign exchange spreads I would incur using my bank-issued credit card. However, its policy of continually reducing its pricing seems to have made its existing customers very evangelical in telling their friends and associates about it, which has helped to fuel its growth.

Of course, not all companies are price-setters. Companies producing commodities such as oil or gold or iron ore are essentially price takers, pretty much getting the market price for whatever output they can produce. However, even these companies will often sacrifice near-term profits to supply commodities to long-term customers at below market prices, particularly where those customers have made a long-term commitment to take a certain quantity of output each year. For example, iron ore producers will agree to long-term supply arrangements with steel companies. While these sorts of arrangements reduce the commodity-producers’ profitability during boom times, they do ensure that they get to sell most of their output at better-than-spot-market prices during any market trough.

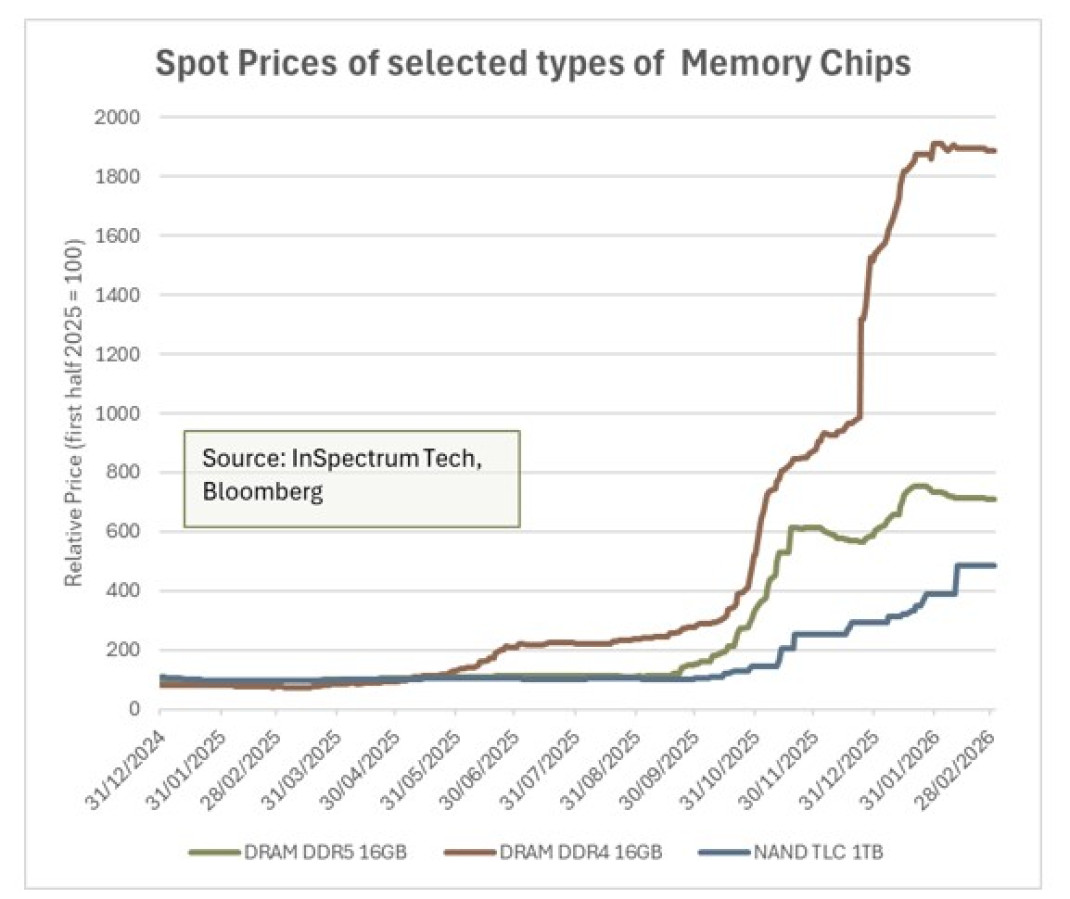

A current example of this involves 3 companies producing a sophisticated form of technology that physically might seem to be the polar opposite of commodities that you dig out of the ground, but nonetheless can trade in a very similar manner to physical commodities – memory chips. Many of the NAND and DRAM memory chips produced by Samsung Electronics, SK Hynix, and Micron (which collectively dominate the market for DRAM and NAND) are interchangeable with each other, and it is therefore possible to observe the spot price for these chips on a daily basis.

The spot prices of DRAM and NAND have risen by an average of about 8-fold from the levels that prevailed in the first half of 2025, and if we mechanically calculate the profits that these companies would make in the first half of 2026 if they were to fully capture this 8-fold increase in price, we should expect some extremely strong profits. For example, I calculate that the increase in memory pricing would theoretically imply an almost USD 200 billion boost to Samsung Electronics’ pre-tax profits in the first half of 2026, which would be enough to make Samsung Electronics the most profitable company in the world. However, it seems inevitable that Samsung Electronics (and SK Hynix and Micron) will look after their good customers a lot better than that, maybe delivering these customers most of their regular volumes at prices that are “only” 2 to 3 times as high as the prices that were prevailing a year ago. They will get the full benefit of high spot prices for some of their remaining output (including a lot of the memory going into data centres), but this may only represent a small proportion of their total revenues.

In choosing not to exploit their customers to the maximum extent possible, the memory chip makers are choosing a similar trade-off to the strategy that Costco takes when it chooses to sell its goods on very low mark-ups – they’re sacrificing short-term profitability in exchange for a better long-term relationship with their customers. However, the duration of their sacrifice will probably be a lot shorter than it is for Costco, as memory chip prices follow a boom/bust cycle, and may drop over the next 3 years as a lot of new memory chip fabrication plants will start production over this period (being built by the 3 companies that dominate the memory market). The demand/supply balance for memory chips could be further affected if the massive demand for memory from the data centre building boom beings to taper off.

The phenomenon of companies with strong market shares choosing not to fully exploit their pricing power is common in the semiconductor industry, where a lot of sub-markets are dominated by just one or two companies. For example, Taiwan Semiconductor Manufacturing Company (“TSMC”) dominates the high-end foundry market (as other participants such as Samsung and Intel have failed to match TSMC’s high yields and are therefore regarded as less reliable partners than TSMC), but it deals with excess demand by rationing the amount of capacity it supplies to each customer rather than gouging them on price.

An even more extreme concentration of market power in another part of the semiconductor industry sits with ASML. ASML is the only producer of the extreme ultraviolet (“EUV”) machines that are used to make high-end semiconductors, and in theory has almost unlimited pricing power, but it chooses to “only” sell its machines for about twice the cost of producing them (~US$400 million) even though it could arguably get away with selling slightly fewer machines at a much higher price (US$1 billion?) if it wanted to maximise near-term profits.

Apart from driving growth, another logical reason why companies choose not to maximise their pricing power in the short-term is to avoid creating a window for competitive entry. Costco sells its merchandise so cheaply that no other retailer would even consider a strategy of trying to out-compete them on price. By looking after its customers, TSMC ensures that they are reluctant to take the risk of shifting production to Samsung or Intel. And by avoiding price-gouging, ASML ensures that its customers are cautious about taking the risk on Canon’s new Nano Imprint Lithography machines, which have the potential to supplant ASML’s EUV machines for a lot of use cases.

In contrast to the restraint that ASML and TSMC show by avoiding price-gouging their customers, it is not so clear to me that Nvidia is showing a similar level of restraint. All of Nvidia’s GPUs are produced by TSMC on ASML’s machines, but Nvidia makes far more profit out of these chips than ASML or TSMC. While ASML and TSMC both sell their output at slightly over twice the cost of production (resulting in very healthy operating profit margins of 37% and 51% respectively), Nvidia sells its datacentre GPUs at about 5 times the cost of production and is generating company-wide operating profit margins of over 60% (overall, Nvidia is selling its output at 3.5 times the cost of production, but will be taking a lower markup on gaming chips and networking equipment than it is with datacentre GPUs).

One consequence of Nvidia’s more aggressive approach to pricing is that it is facing a much higher level of competitive entry than TSMC or ASML. Companies like Alphabet (Google), Microsoft, and Amazon are trying to reduce their reliance on Nvidia by building their own chips, and many startups are developing chips that can be used for AI training and inference. Nvidia’s strategy is certainly producing greater near-term profits than the more restrained approach taken by TSMC and ASML, but there is a risk that these high profits will come at the cost of a loss of market share over time.

How do we distinguish the “price gougers” from the “loss leaders”?

From an investment perspective, it makes sense to pay higher earnings multiples for companies that are clearly sacrificing current profitability to fuel or protect future growth, and to require lower multiples for shares in companies that are maximising near term profitability by harvesting / gouging their existing customer base.

It is not always straight forward to determine where a company sits on the continuum that stretches from “loss leader” (keeping prices low to fuel growth) to “price gouger”, but some of the key indicators we can look at include the following:

- Is the company gaining new customers or losing existing customers?

- Is the company gaining or losing market share?

- Do customers feel that they’re getting a good deal from the company? Or do they feel like they’re being over-charged?

- If the company were to increase its prices by (say) 10%, how would this change customer behaviour?

- How high are the company’s gross profit margins, operating margins, and returns on invested capital?

- Are new companies entering the market, and looking to win customers based on a better value proposition?

Overall, it will be an encouraging sign if your answers to most of these questions imply that a company is looking after its customers, but a worrying sign if most of the answers support a view that it is gouging them.

Investing in companies that are prioritising short-term profitability ahead of longer-term resilience and growth is generally a risky proposition, regardless of whether the mechanism for boosting short-term profitability is charging high prices, cutting back on research & development expenditure, pursuing unethical business practices, accepting business from dodgy clients, or compromising on things like customer safety. It is generally safer to invest in companies that behave responsibly and don’t over-charge their customers.

As value-orientated investors, we like to compare the price that we’re paying for a business to the profits that it is currently generating, but it is important that we consider those profits in the context of the decisions that the company has made which could be either boosting current profit at the expense of future growth or reducing current profitability in exchange for a healthier long-term outlook.

Nicholas Bagnall is Chief Investment Officer at Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited and an investor in Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including Te Ahumairangi Global Equity Fund) that invest in global equity markets, and hold shares in companies mentioned in this article, including Paypal, Adobe, Microsoft, Wise, Samsung Electronics, TSMC, Canon, Nvidia, Alphabet, and Amazon.