The Importance of Beholding Earnings (expectations)

NBR Articles, published 7 April 2026

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 7 April 2026.

Numerous broker analysts publish estimates for the future earnings, cashflows, and balance sheets of large listed companies. Working as a professional fund manager, I can access the detail of these forecasts through broker research portals and through a Bloomberg terminal. But anyone with access to the internet can also access quite a bit of information about the average analyst earnings expectation through free online services such as Yahoo! Finance.

There are of course many different ways you can use this data. The most traditional approach is to evaluate stocks based on a price / earnings ratio (“P/E”) calculated by dividing the stock’s price by estimated future earnings per share. However, when used in isolation this approach has not worked very well in the US over the past 20 years (except in helping to eliminate the most egregiously overpriced stocks from consideration): the stocks that were cheapest using P/Es based on analyst estimates for future earnings have performed slightly worse over the past 2 decades than stocks that were middle-ranked using P/Es calculated from analyst estimates (although both groups outperformed the stocks that were most expensive based on forward P/Es).

Further, back-testing shows that selecting stocks based on their multiple of expected earnings has generally not worked any better than the simpler approach of selecting stocks using a price/earnings multiple calculated based on trailing (historical) earnings.

Given this observation that P/Es based on analyst expectations work no better than P/Es based on published historical earnings, you could be excused for wondering whether there is any point in paying any attention to analyst expectations.

However, analyst expectations for company earnings have historically proven to be useful tool for picking stocks, provided that you pay attention only to the direction in which analysts are revising their earnings expectations, whilst generally ignoring the absolute level of earnings that analysts are expecting and the growth rates that they expect each company to achieve.

In simple terms, the rule is that you should generally favour investing in those companies for which analysts have been revising up their expectations for future earnings and should be wary about holding shares in companies where analysts have been revising down their expectations for future earnings.

The first academic research showing that analyst earnings revisions helped predict stock returns was published in 1979, but this finding was not well-known until the 1990s, when Richard Bernstein and other market strategists started writing about the power of earnings expectations. Bernstein described it as the “cockroach effect” (well before Buffett used the same term in a different context) based on the observation that, in common with cockroaches, the appearance of single earnings revision generally indicates that you should expect to see a lot more revisions (in the same direction) over the comingweeks.

The trend in earnings revisions worked very well as a stock selection tool in the decades prior to people becoming aware of its power towards the end of the 20th century. This was due to (1) the fact that over those periods the market had typically under-reacted to earnings revisions and (2) there is a tendency of earnings revisions to follow a trend.

A real life example of earnings revisions…

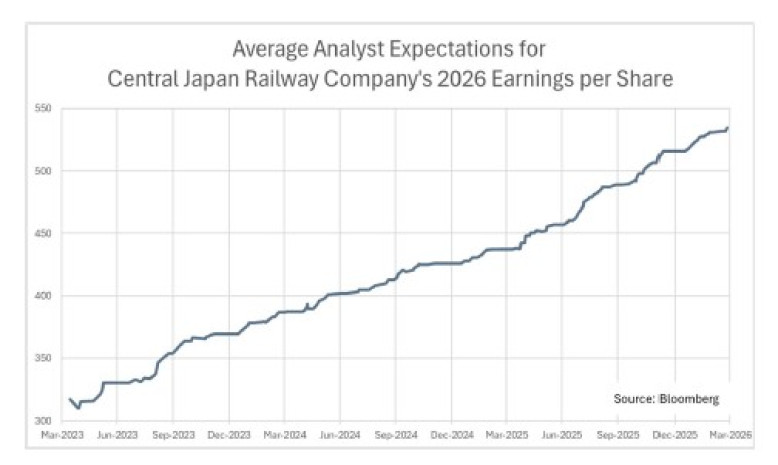

It is not uncommon to see earnings expectations for a company continue to trend in the same direction for several months, or even years. For example, in the graph below I show that earnings expectations for Central Japan Railway have trended upwards over the past 3 years. This company’s earnings are driven mainly by patronage of the Shinkansen bullet train between Tokyo and Osaka, and in 2023, the consensus expectation had been that patronage would remain well below pre-covid levels. Each month, as more data came out showing that patronage was growing, analysts seem to have begrudgingly lifted their expectations to reflect the growth-to-date in Central Japan Railway’s patronage, but each time they essentially assumed that there was no ongoing trend, and the growth would stop from that point forward. Even now, after 3 years of lifting their expectations, it would seem that analysts remain too conservative, forecasting that earnings will be lower in the March 2026 quarter than they were in the March 2025 quarter, even though the company has released data showing that up until the 25th of March, passenger volumes were running 5% higher than in the same quarter of the previous year.

When earnings expectations stopped working in the United States

Although earnings expectations had worked so well as a tool for picking stocks over the period up until the late 1990s, they stopped producing consistently positive results in the United States once everyone became aware of the “cockroach effect” (i.e. how well earnings revisions had historically worked as a stock selection tool). We can see this in the graph below, which shows Citigroup’s factor index for the “earnings revision factor” in the United States.

This graph shows that investors who had been systematically buying shares in companies with the best earnings revisions and shorting the shares of companies with the worst earnings revisions would have suffered a big loss during the “tech wreck” of 2000 to 2002, as well as a further loss during the recovery out of the GFC, and even today they would have still not have fully recovered these losses. Since people became aware of the “cockroach effect” with earnings revisions (shortly after the start of this graph), the incremental returns that US investors have got from paying attention to earnings revisions has been no better than they would have got from tossing coins.

What changed? I see two key changes that destroyed the profitability of selecting stocks based on earnings revisions after the 1990s:

1. When investors became aware of the power of earnings revisions, they stopped ignoring earnings revisions and started reacting immediately to new information (e.g. earnings results) that would lead to earnings revisions. As a consequence, the share market’s response to earnings announcements transitioned quickly from shrugging to panicking. In New Zealand, I can remember an era when it was often possible to grab large blocks of stock at the same bid or offer at which they had been proffered prior to a game-changing earnings result. This all changed as people became aware of the power of earnings revisions, and in a short period of time the market completely transitioned towards a tendency of delivering extreme share price reactions to even relatively small beats or misses in reported earnings.

2. The regulations governing how companies interacted with analysts tightened up. In the “bad old days” company management would often discuss current trading performance with whichever analyst happened to be visiting them, without seeing the need to announce anything to the market. Accordingly, a single earnings revision would often indicate that an analyst had got the “inside scoop” as to how a company was trading. As regulators started to investigate and/or prosecute companies for selectively releasing information to the market, behaviours changed, and it therefore became much less likely that an earnings revision was indicative of any non-public information about how the company was trading.

Interestingly, while earnings revisions seemed to stop working as a stock selection tool in the United States after the 1990s, they continued to be a good tool for selecting stocks across developed markets generally, as shown in the following graph showing the performance of Citigroup’s earnings revision factor for developed markets. The upward slope of this graph indicates that in a global context, paying attention to earnings revisions has continued to assist with stock picking over the past 30 years.

Why have earnings revisions worked so well in the developed world as a whole, despite adding no value in the largest single market (the United States)? The following points help explain the difference:

1. Earnings revisions have continued to be a good indicator of future stock performance in Europe and Asia-ex-Japan. One factor contributing to this may have been that these share markets often show relatively muted share price reactions to new information (in comparison to the more extreme share price reactions that we sometimes see in markets such as Australia or the United States).

2. It is also possible that selective dribbling of information to analysts remains a factor in some markets that do not enforce insider trading and continuous disclosure rules as strictly as the US.

3. It would seem that earnings revisions would have helped inform allocations between countries, implying that the share markets of countries have seen a lot of earnings expectation upgrades generally outperform the share markets of countries with a recent predominance of earnings expectations downgrades.

When should you pay attention to Earnings Revisions?

Clearly, history shows that paying attention to earnings revisions has often been a very valuable complement to investment decision making, but that it has not always added value, as we can see from the poor performance of Citigroup’s Earnings Revisions factor index for the United States in the current millennium (and in particular over the 2000-2002 period, and during the 2009 bounce-back from the GFC).

Accordingly, it makes sense to be selective about how you pay attention to revisions to earnings expectations. I would suggest that the following rules will help investors know when to pay most attention to earnings revisions:

1. Paying attention to earnings revisions has worked on average over time because markets have often under-reacted to new information that informs the future outlook for a company’s earnings. If you find yourself in a market environment where the market often seems to be shrugging off new relevant information, it is probably sensible to lean heavily towards avoiding companies experiencing earnings downgrades while favouring companies experiencing earnings upgrades. But if you’re in a volatile market where share prices are seemingly reacting in extreme ways to relatively minor scraps of new information, you probably avoid allowing your investment decisions to be too heavily influenced by the direction of earnings revisions.

2. Earnings revisions are more relevant if they point to a shift in a company’s underlying earnings power, and less relevant if they simply reflect shorter-term influences on profitability. It therefore makes sense to pay more attention to earnings revisions that are driven by companies gaining market share and acquiring more recurring customers, but to pay less attention to earnings revisions that are due to one-off gains or losses (e.g. gains on sale or restructuring costs) or income from “lumpy” income streams (e.g. investment banking income, trading income, or income from large construction contracts).

Related to the second point, I prefer to look at how analysts are revising their earnings expectations for a company’s earnings two years into the future rather than revisions to the current year’s earnings, as revisions to current year’s earnings often include a large element of “noise” due to one-off items.

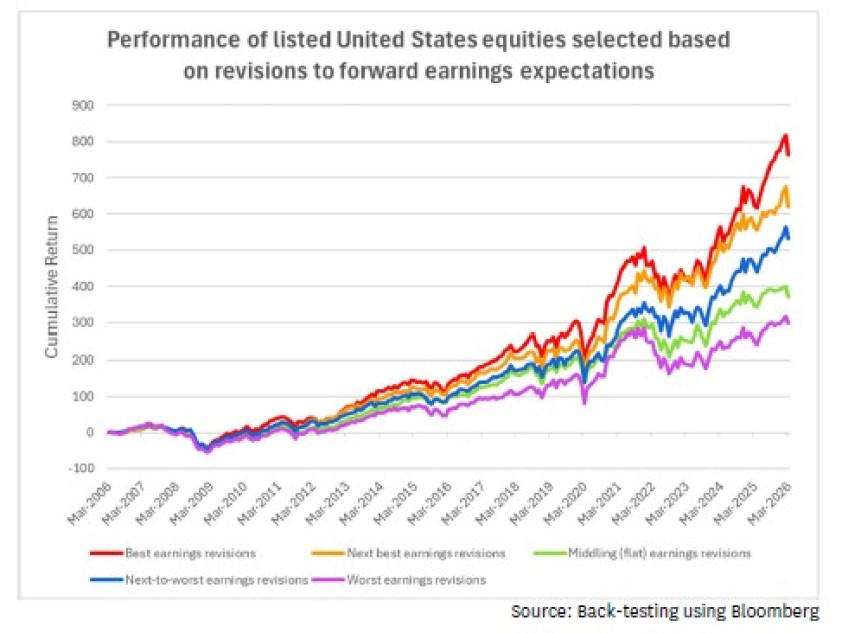

When I back-test the performance of earnings revisions for picking stocks using expectations for the earnings 2 years into the future, I get more consistently positive results that we see from the Citigroup factor indices. For example, the following graph shows the performance of US stocks (in the MSCI US index) sorted into quintiles based on the rolling 4-week change in expectations for earnings 2 years into the future.

As can be seen, investing in the stocks with the best trailing earnings revisions (for earnings 2 years ahead) has produced the best results over time, investing in the stocks with the next-best trailing earnings revisions has produced the next-best investment results, while investing in the stocks with the worst trend in earnings revisions would have produced the worst investment results. However, one divergent result is that companies with only a mildly bad earnings revisions trend have actually produced better investment results than companies from the middle bucket for earnings expectations.

(Note that for most months in the back-test sample, the “middle bucket” consisted of all the companies for which there was absolutely zero change in average earnings expectations over the preceding 4 weeks).

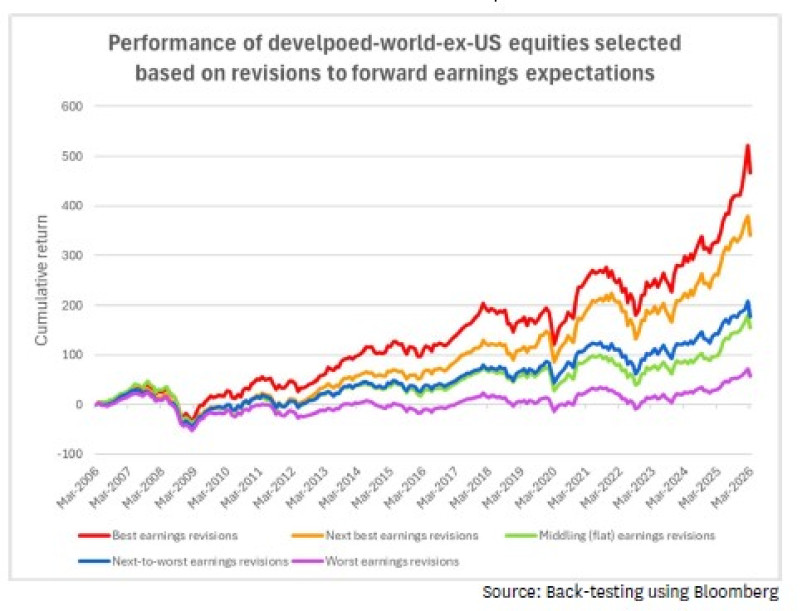

The graph below shows that we get similar results when we apply the same screening criteria to companies from developed markets outside the United States.

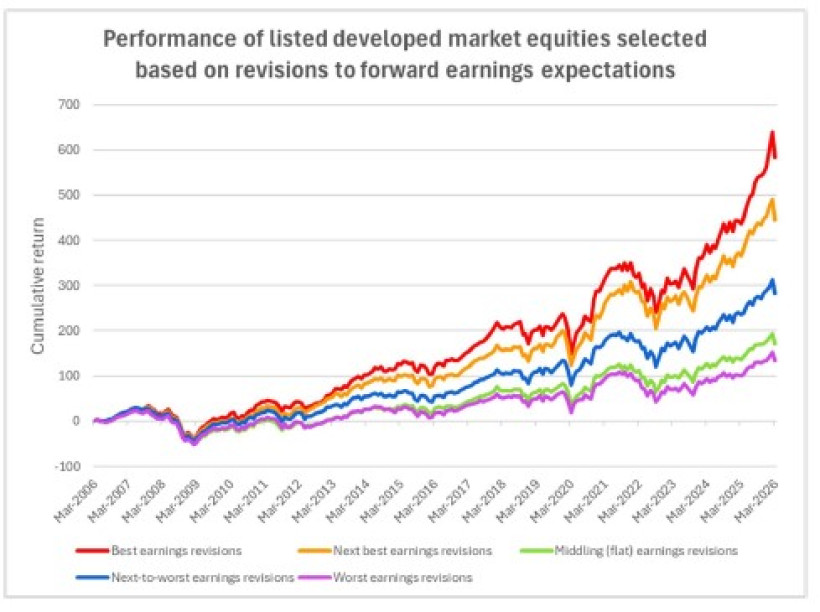

Unsurprisingly, we also get similar results when we select stocks from the MSCI World universe based on revisions to 2-year-ahead earnings forecasts:

In summary, the trend in earnings revisions can be a powerful tool to overlay to an investment process, particularly if you pay attention to what the earnings revisions indicate about changes in each company’s underlying earnings power, and don’t over-emphasise earnings revisions during periods when a market is showing a tendency to over-react to new information.

Nicholas Bagnall is Chief Investment Officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios include investments in Central Japan Railway Company, which was mentioned in this article.