Old Birds, New Tricks

NBR Articles, published 12 May 2026

This article, by Te Ahumairangi Research Analyst, Prithvi Sharma

originally appeared in the NBR on 12 May 2026

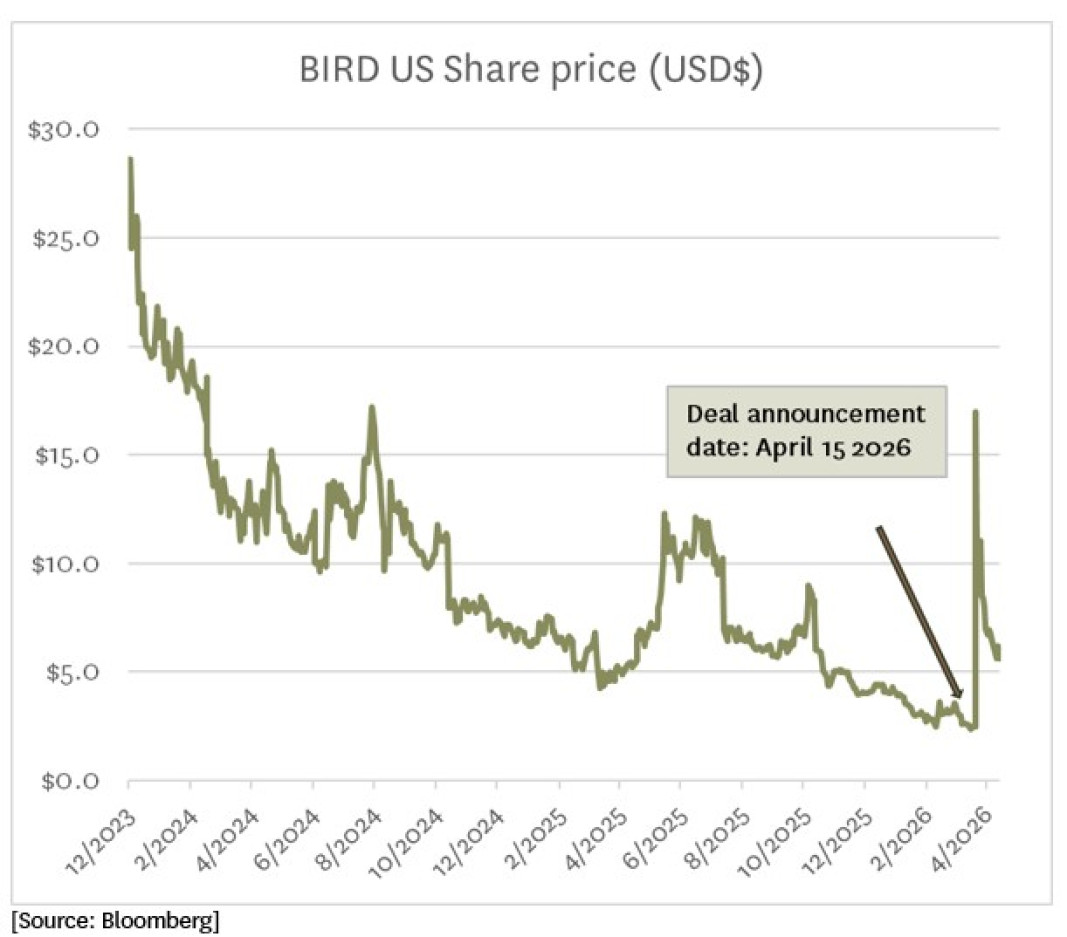

They say a tiger cannot change its stripes. Such restrictions need not apply to birds it seems, or at least not to publicly listed ones. With its shares having fallen in value by over 90% from its 2021 IPO price, those who still owned Allbirds shares could be forgiven for likening the overnight transformation from formerly trendy sneaker brand to currently trendy GPU-lessor ‘NewBird AI’ and the accompanying five-fold investment return to that of the mythical phoenix, rising from its ashes.

The Phoenix, of course, is the namesake of Wellington’s A-League football team, for whom Allbirds co-founder Tim Brown played as a founding squad member. The metaphor couldn’t be more convenient. Outside of Wellington, the transformation must only have been more surprising on the west coast of the United States where the firm is headquartered and where its flagship ‘Wool Runner’ was once a beloved component of the tech bro uniform, treasured for its comfort, sustainable sourcing and casual aesthetic.

But perhaps the surprise was closer to amusement seeing as this wasn’t even the first Bird-to-AI company overhaul to hit Silicon Valley. That title belongs to Elon Musk’s 2022 acquisition of Twitter in which he erased the bluebird logo, renamed the platform ‘X’ and then folded the enterprise into xAI which produces the Grok lineage of AI models. Allbirds to NewBirds might be more disorientating, however, in that the product change was less about shoes or even AI and more about the listing.

Steady progress or switcheroo

New Zealand investors have seen versions of this before. Plus SMS is a local cautionary tale, a back-door listing into the market at a time when mobile messaging was the market’s favourite new technology - the company was once valued at around $240 million. The shares last traded at half a cent, and the company was later delisted after repeated governance breaches and financial distress. The case makes for an eerie precedent where a listed vehicle meets a fashionable theme. Other backdoor listing attempts to catch the slipstream of a fad in vogue that New Zealand investors may be familiar with include:

- ihug’s attempt during the dot-com bubble, and

- Geneva Finance & MFS in 2005 when finance companies were still fashionable before the GFC.

To be sure, corporate history is littered with reinvention and it is likely a required capability for firms expecting to sustain themselves in the long run. Nokia began as a paper mill before becoming a household name for its durable phones. Today, its investors are far more interested in its datacentre optical products. Amazon famously was once just a bookseller, and some might be surprised to hear shares in Blackberry, of early 2000s mobile fame have almost doubled since March. And no, it doesn’t sell Blackberry phones anymore. The common theme among these pivots is the evolving nature of technology.

Becoming NewBird AI was more of a radical departure than an incremental evolution, however. They sold shoes, really popular ones - comfortable and beautiful but as is often the case with single product phenomena that capture a moment, moments fade. Peloton, and more recently Pop-mart’s Labubu boom are only the most readily accessible in our memory of consumer darling-to-devil (and sometimes back again) stories that plague the discretionary consumer sector. So, Allbirds realised the need for change and decided that changing its category altogether should be the solution. Its critical asset became its rights as a publicly traded vehicle.

Finessing the funding

A beleaguered private company trying to raise money to reinvent itself generally has to subject itself to a lot of scrutiny. It must persuade a small group of investors, survive often harsh due diligence, and live with the terms that sophisticated investors are willing to agree to. Already listed companies have a different ruleset. A change of name, fresh press release and investor deck might be all that’s required to generate the capital it needs if it uses the right words. Today, retail traders can buy from an app on their phone, an initial share price reaction can trigger fundamentally apathetic trend-following funds that may be eager to pick up a new name that fits their investable universe. This is an enormous, effectively infinite pool of capital to draw from when your starting capitalisation is on the order of tens of millions of dollars.

Imagine if NewBird AI had been formed privately. A newly incorporated GPU-leasing company with no operating history, no perceivable procurement advantage, and no hyperscale infrastructure would probably not be able to raise money by selling investors on the trend of AI alone. Now imagine if they tried to IPO. It would be difficult to even try to do so with the scant disclosure around their new operations available today, investors would be demanding to know: ‘what exactly are we being asked to finance?’

The answer, at least from the first disclosures, looks less like a Neocloud platform like Coreweave and Nebius and more like a small equipment-finance business. NewBird AI struck a deal with an anonymous private financier and used proceeds from the initial convertible-note tranche to buy server equipment containing current-generation Nvidia Blackwell GPUs. They have arranged to lease those assets to QumulusAI for approximately US$2.75 million over three years, with an end-of-term purchase option. The filing does not disclose the precise purchase price, hardware configuration, or option terms. Of the headline US$50 million financing facility, the initial committed note tranche was only US$5.25 million, subject to a 5% original issue discount, which gives a reasonable proxy for the scale of capital involved. Among other curious aspects, the facility can be converted to equity at several favourable prices for the investor including the preannouncement price and the interest rate on the facility is 12%.

A simplification of the initial economics might look like this:

- Note principal: US$5.25 million

- Cash received by NewBird after 5% original issue discount: roughly US$5.0m

- Lease revenue over three years: US$2.75m or US$0.92m per year

- Financier’s coupon: 12% per year x US$5.25m = US$0.63m per year

Starting with the financier’s claim. The note carries a 12% coupon, but the first wrinkle is that it matures in just two years, creating a duration mismatch with the three-year lease. On US$5.25m of principal, two years of simple interest implies interest costs of US$0.63m x 2 = US$1.26m. Assuming the lease revenue is earned evenly, the first two thirds of the lease revenue they would have earned from their contract with Qumulus would have only generated US$1.83 million by then, leaving less than US$300,000 dollars each year for overheads and general operational costs required such as collocation rent and energy before the facility of US$5.25m is required to be repaid in full.

Even if we assume this issue can be easily resolved the initial terms ensure the financier will get at least U$7.14m and Newbird, in the best case, is getting just US$2.75 million for its GPU rental service. That leaves the listed vehicle $4.39m dollars short.

For simplicity, we are ignoring the effects of time-discounting which exacerbates the nominal economic requirement of the residual value but in the most generous case, for equity investors not to be underwater on this transaction, the server equipment purchased would need to be worth at least 90% of the initial purchase value, in three years’ time. This may be a difficult proposition for NewBird AI to pull off, even if they did have a proven track record, given the rate of improvement between GPU generations is on the scale of an order of magnitude or more depending on how one chooses to measure it.

Competition for compute is cruel

Equipment finance can be a good business when the owner has cheap capital, scale, procurement relationships, customer access and a stable view on the resalable value of the product being leased over time. Without keen specialisation or a heavily consolidated, uncompetitive market, financing rarely delivers a return to its operators sustainably higher than its cost of capital. The problem for Newbird AI is that if its prior management found competing in the sneaker business hard going, its new competitors in AI compute are the ‘Hyperscalers’ (Amazon’s AWS, Microsoft’s Azure, Google Cloud). That term says about everything NewBird AI needs to know about those companies’ competitive advantages, across technology and finance.

Unfortunately for NewBird AI A class shareholders, they cannot simply label the situation ‘high risk, high reward’. The private financier has a convertible option that allows for conversion at their discretion. If stockholders approve the measure to bypass Nasdaq's 19.99% issuance limit, the financier can convert their debt into shares at a discounted, floating 'Alternate Conversion Price' which would be enormously dilutive to existing investors even in the upside case.

Even more so than AI, cryptocurrency is the breeding ground for peculiar investment vehicles and creative financing strategies for assets that may or may not be worth anything in the near future. Special-purpose acquisition companies or SPACs are often the mechanism of choice today for private businesses looking to enter public markets without the scrutiny of an IPO (although the managers of such SPACs typically promise to undertake proper due diligence before undertaking any acquisition) and many of these examples are some form of crypto-currency business often miners or exchanges. Another peculiar analogue is (Micro)-Strategy, which rather than gaining a suffix like NewBird AI, lost its prefix and similarly has been known to engage in a convoluted financing arrangement. In Strategy’s case it has convinced investors that its Bitcoin treasury strategy is so impressive that it should trade at a premium to the Bitcoin it owns through which it can profitably issue shares and use the proceeds to buy even more bitcoin! NewBird may be taking notes.

How NewBird AI will turn out is anyone’s guess but for all that is spoken about private equity and private credit today, there seems to still be plenty of allure for crafty financiers to engage with listed markets when the time and theme is right. As an owner of a pair of Wool runners, I must admit I preferred the shoe company, but what is clear to me is whoever coined the phrase ‘you can’t teach an old dog new tricks‘, had never tried plugging a NewBird into a GPU.

Prithvi Sharma is an Equity Analyst at Te Ahumairangi Investment Management.

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is an employee and shareholder of Te Ahumairangi Investment Management Limited. Te Ahumairangi manages client portfolios that invest in global equity markets, and hold shares in the following companies mentioned in this article: Amazon, Microsoft, and Alphabet (parent company of Google Cloud).