Will the market share your bullish views when the tide goes out?

NBR Articles, published 26 March 2024

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 26 March 2024.

More than has been the case in any other time that I have experienced (in 31 years of equity analysis and portfolio management), the language that equity analysts and other market participants are using to communicate their ideas is short-term in nature. Rather than expressing their views in terms of the returns that investors might expect from investing in a company’s stock over a longer-term time period (such as a decade), analysts communicate their ideas almost exclusively in terms of “price targets”, representing an expectation of where they guess the stock will be trading at the end of the year or in one year’s time.

When we look into how analysts have arrived at their price targets, we generally see that the “price target” is simply calculated by a applying a multiple to the analysts’ expectations for earnings or cashflows over the next one or two years, with that multiple often linked to the multiple at which the stock currently trades, or to the average multiple at which it has traded over the recent past. Historically, analysts would often calculate their price targets based on a discounted cashflow analysis (therefore ensuring that the short-term price target was linked to a longer-term view), but this approach now seems increasingly rare, particularly in the US market.

The Greater Fool Theory

Selecting investments based on short-term views about where a stock price is headed (without any anchoring to longer-term valuations) is often described as the “Greater Fool Theory” – you’re buying a stock without knowing what it is worth, but you’re optimistic that someone even more foolish than you will pay a higher price for it in the future.

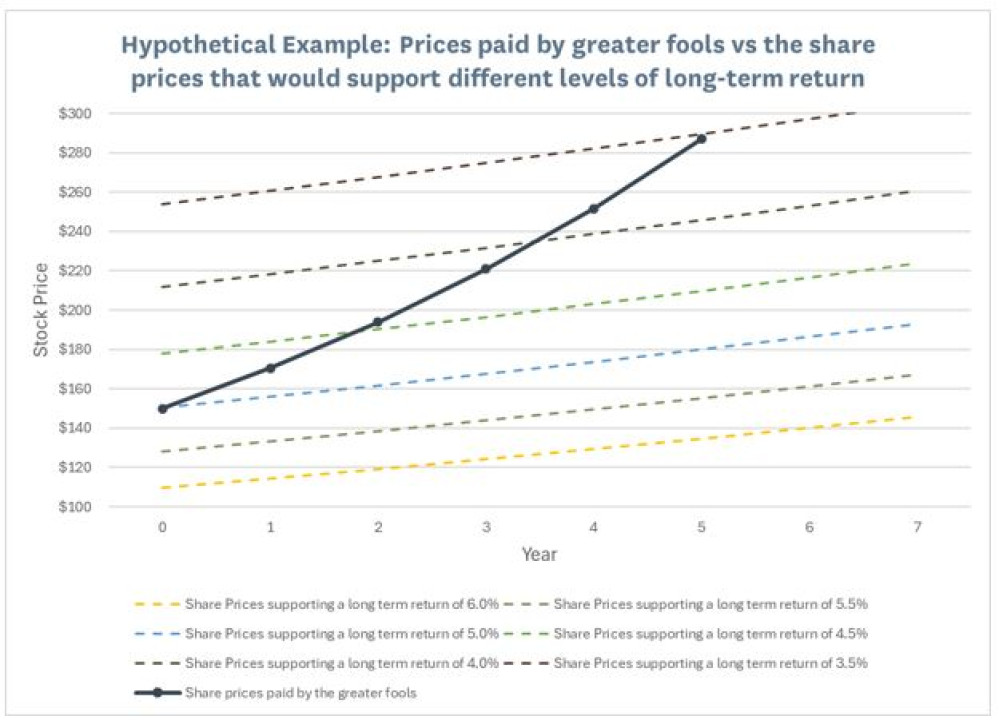

In truth, the stock might be priced so expensively that it can only deliver a long-term buy-and-hold return of 5% per annum from the price you paid, but it is still conceivable that you might enjoyed a 15% return over one year if a “greater fool” then buys the stock off you at a price that can only support a long-term return of 4.75% per annum. And if that punter manages to sell the stock to an even greater fool at even higher multiple of earnings after a further year, then they may also achieve a 15% return, provided that the greater-greater fool who buys the stock off them pays a price could only support an even lower buy-and-hold return of (say) 4.45% per annum.

I attempt to illustrate this in the graph below, where I show a hypothetical example of how a succession of punters could pay ever increasing prices for a stock. The prices that each punter pays is only consistent with modest long-term returns (5.0% in year zero, falling to 3.5% by year 5), yet (under the scenario I have constructed) each so-called “fool” achieves 15% returns (including dividends) from on-selling their shares to an even greater fool.

This application of the greater fool theory plays often out well for the “fools” in a bull market, where a continual inflow of funds into the market may push up the share prices of most companies that are reporting some sort of earnings or revenue growth.

In this bullish market environment, investors can get used to buying stocks on multiples of as high as 50 times current earnings, and they may enjoy strong returns from those stocks as long as (1) the bullish market environment persists, (2) those earnings continue to rise, and (3) the stocks they’ve bought maintain or expand their elevated earnings multiples.

So what happens when the bull market ends?

With enough optimism you can always justify a high share price

It will not immediately be evident to most people playing the “greater fool game” that the prices they are paying for shares are unlikely to deliver acceptable long-term returns, because it will almost always be possible to make a semi-plausible long-term argument that back-solves to justify a particular company’s share price.

Even in late 2021 when Tesla was being valued at more than 20 times annual sales, and all significant car manufacturers were entering the electric vehicle market, more broker analysts had “buy” recommendations on Tesla than “sell” recommendations. While many of these buy recommendations started and ended with a price target that applied then-current multiples to an (ultimately correct) expectation that Tesla would make more money in 2022 that it had in 2021, those analysts who did feel some obligation to talk about the longer term outlook invariably projected that Tesla would take a huge share of the world automotive market over the next few years whilst sustaining profit margins that were much higher than indicated by all precedents for the automotive industry.

This was consistent with a historical pattern of equity market analysts building forecasts that justify current market prices. Even if a company’s stock is trading on 50 times earnings whilst it is distributing no cash to shareholders, a bullish analyst would always be able to construct an argument that goes something like this: (a) it’s exceptional prospects mean that its earnings per share will growth 7-fold over the next decade; (b) that the company will then be able to distribute 60% of its earnings to shareholders while continuing to grow earnings per share at 5% per annum for the following 4 decades; and (c) that even in 50 years’ time, the market will still value the company on 30 times earnings. If you believe all of this, you could anticipate a compound return of 10.2% per annum from investing in the company’s stock and holding it for the next 50 years.

These are the sorts of mental gymnastics that bulls on Nvidia, Amazon, or Tesla will perform if you try to get them to justify how their favourite stock might provide an acceptable risk-adjusted return over the long term. Such scenarios for the future earnings of these companies may be possible, but are they likely?

Forecasting is difficult

Niels Bohr is reputed to have said “Prediction is very difficult, especially if it’s about the future!”. But even within the subset of “predictions about the future”, we can differentiate between different classes of forecast that have varying degrees of reliability.

At the top end of forecast reliability, I would argue that we can generally be more confident in forecasting that things that have been occurring for a long period of time will continue to occur in the future (particularly if there is no question of the sustainability of that activity). So, for example, we can be pretty confident that the sun will rise each morning, water will be delivered to homes via pipes (even in Wellington!), that electricity will continue to be delivered via electricity networks, and that people will continue spend money on things such as food, clothing, housing, entertainment, etc.

Next on the hierarchy of forecast reliability, we might sensibly project that long term trends may continue for some time (for example, real GDP per capita will keep growing at between 1% and 2% per annum in developed economies, or that birth rates will remain low in developed countries). We may also feel pretty confident about predicting that more recent trends may persist for at least a few years, albeit with a gradual slowing over time (for example, the growth of the public cloud or the growth of streaming video services).

However, forecasts for exceptional growth prospects rightly belong at the bottom of the hierarchy for forecast reliability. It will typically require exceptional confidence (or stupidity) to forecast that an already large company will achieve 7-fold growth in revenues and profits whilst achieving exceptional returns on capital, because to make this forecast, you are essentially taking a view that you can see an opportunity for the company that its potential competitors must be blind to.

If there truly is a foreseeable opportunity for Tesla to sell 7 times as many cars as it is today while continuing to earn high margins and high returns on capital, then shouldn’t we assume that many other automotive manufacturers will see the same opportunity and compete for it, therefore driving down returns? Similar logic applies to Nvidia and GPUs. If the demand that AI is creating for GPUs and other AI-enabling chips is as large as implied by Nvidia’s share price, then won’t semiconductor companies also see it, and continue to go full speed ahead on developing competing chips, which should ultimately result in future margins on GPUs being much lower than they are today?

Of course, counter-arguments can be made to the effect that Tesla and Nvidia have some unassailable technological leads that their competitors will never catch up with. The proponents of such beliefs seem to have difficulty explaining these technological barriers to future competition in a language that ignoramuses such as myself can understand. Maybe this says more about my inability to comprehend than the strength of these company’s technological leads over their competitors, but regardless of whether it is their arguments or my understanding that is weak, I think it is worth considering how the market will price such bullish conjectures in the event of a market meltdown.

What happens to different share prices when the market sells off?

Forecasts grounded in the expectation that “things that have occurred in the past will continue to occur in the future” do not tend to be hugely shaken by sudden swings in investor confidence. If the market crashes and investors start to question everything they previously thought they understood about the world, then the share prices of companies that depend on the assumption that “stuff we are used to will continue to occur” may fall slightly, but they won’t crash. For example, the price/earnings multiple of a regulated electric utility might drop from 14 times to 13 times, but the implicit loss of 7% of market value would represent a relative safe haven during a market crash.

Rather, when investor confidence takes a tumble, the share prices that fall most will be those that are most dependent on conjecture about the future. In the current market environment, these will be share prices that are inflated to several times the value that you might infer for the company based on a continuation of its current profitability. These inflated share prices are boosted by optimistic expectations for future growth, but as such expectations typically rely on untestable assumptions about the future, and as history shows that investors anticipate exceptional growth from listed companies far more often than they actually get it, these will be the sorts of assumptions that come under the most pressure if investors begin to lose confidence.

The vulnerability of highly-priced growth stocks to share market downturns applies to both those companies where the expectations for future growth will prove to be excessively optimistic, as well as to those companies that will ultimately deliver the growth that the market expects. For example, Amazon has been the stand-out share market performer of the past 20 years, and was also a market darling during the previous tech boom, which peaked in late 1999 / early 2000. While Amazon’s growth over the past 20 years now implies it was a bargain even in December 1999, few people remember that its share price fell 95% between its December 1999 peak and its trough in October 2001.

If the market experiences a significant correction in the next couple of years, I am confident that it would be the highly-priced growth stocks that experience the brunt of the downside. While it is likely that a handful of today’s highly-priced growth stocks will ultimately achieve sufficient growth to justify today’s share prices (just like Amazon did after the previous tech wreck), identifying the winners is not easy, and it is likely that almost every highly priced growth stock (future-winners and future-duds alike) will fall together in the event of a significant market sell-off.

Nicholas Bagnall is chief investment officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios hold shares in Amazon, which was mentioned in this column.