Higher bond yields are a challenge for US equity valuations: Identifying the biggest losers

NBR Articles, published 10 October 2023

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 10 October 2023.

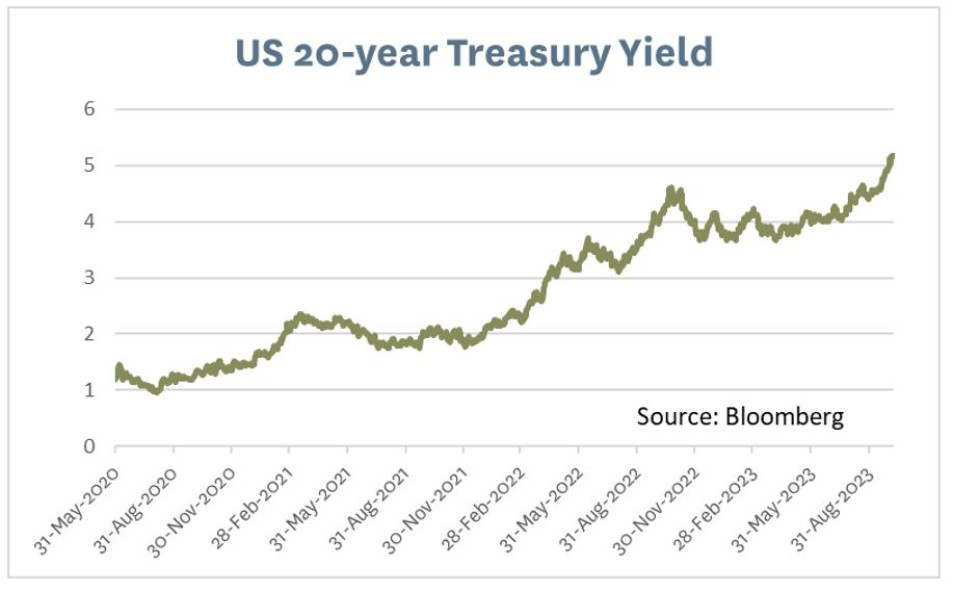

US long-term bond yields have risen about 1.4 percentage points in the last 6 months. About 0.2 percentage points of this rise reflects a rise in long-term inflation expectations, while the remaining 1.2 percentage points represents an increase in real (i.e. inflation-adjusted) interest rates (which can be inferred from a 1.2 percentage point increase in yields on US Treasury Inflation Protected securities). As the graph below shows, bond yields have now risen almost 4% over the past 3 years.

US Bond yields are now higher than the earnings yield on US Equities

This rise in real bond yields severely dents the relative attractiveness of equities. Over the past 6 months, the trailing earnings yield on US equities has dropped slightly, from 4.97% in early April to 4.63% today. Hence, the yield to maturity on 20-year US bonds (5.17%) is now more than 0.4% higher than the earnings yield on US equities.

This is unusual – for most of history, the earnings yield on the US equity market has been higher than US treasury bond yields. This is easy to understand: equities are riskier than government bonds, so investors normally demand some meaningful extra return for the incremental risk of investing in equities.

Earnings yields are a good conservative indicator of future equity returns

The earnings yield on a diversified equity market has historically provided a good conservative indication of the long-term pre-tax return that investors should expect from investing in that market.

In the long term, returns from equities come from the cashflow that equities generate for investors (through dividends and share buybacks) plus growth in the value of the equity market. While only a portion of corporate earnings will be distributed to shareholders, the remaining portion that is retained and invested in growth has tended (on average) to generate a very good return on investment. Hence, this reinvested capital ultimately gets valued by the market (on average) at more than 100 cents per dollar. Taking this into account, it is reasonable to expect that long term returns from an equity market will be slightly greater than indicated by its earnings yield.

Incidentally, the fact that the average company achieves a good return on retained-and-reinvested earnings might be seen as a reason to favour companies that reinvest a high proportion of earnings. Unfortunately, empirical evidence says otherwise, with companies that reinvest a higher proportion of earnings tending to deliver lower returns on capital and lower total shareholder returns than companies that are more circumspect and disciplined about investing additional capital.

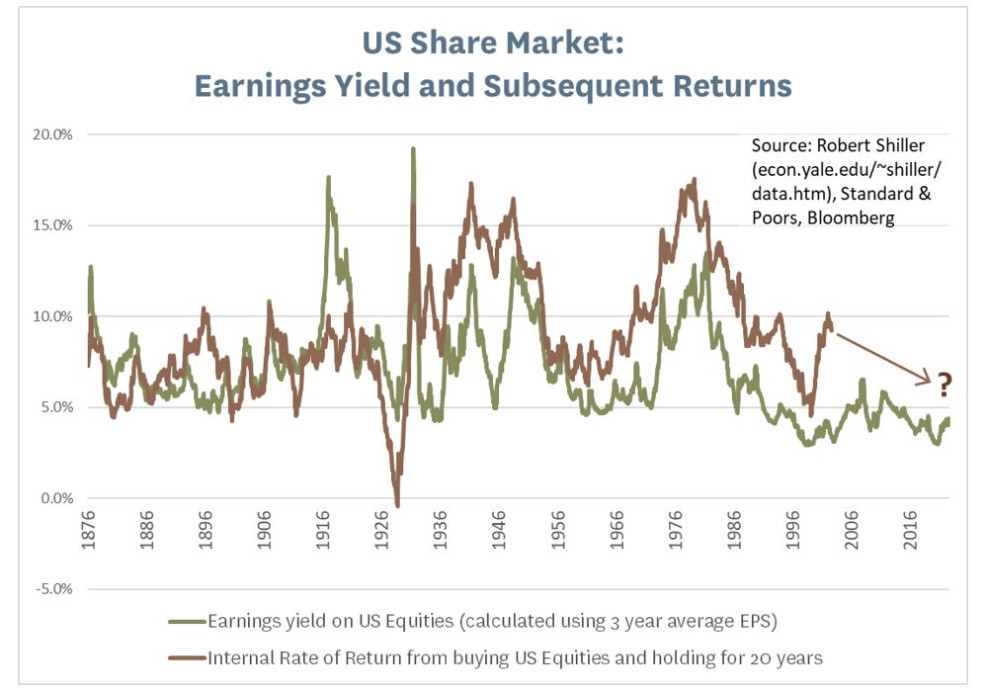

The graph below shows the historical earnings yield for the US equity market, and the subsequent returns that investors would have got (in USD dollar terms) if they’d bought US equities and sold them 20 years later (while keeping the dividends that they received along the way). For this analysis, I’ve calculated the earning yields using a 3-year trailing average of earnings, to avoid having the analysis too distorted by any short-term fluctuations in corporate earnings.

Over this period, the average subsequent return that investors would have received from buying and holding US equities for 20 years was 9.2%, which was on average 1.8% greater than the earnings yield they were seeing at the start of each 20-year period. US inflation averaged 2.7% over these 20-year periods, and the extent to which subsequent equity returns exceeded the observed earnings yield was very correlated to inflation over the subsequent 20-year period (on average, every 1% of extra inflation added 0.81% to the subsequent equity return).

Based on these historical relationships, we could infer the prospect of a pre-tax US dollar return of about 6.2% per annum from buying US equities today and holding them for the next 20 years. This is slightly lower than the 7% long-run return I projected in my February article on allocations to US equities [ https://www.nbr.co.nz/margin-call/untitled-article/ ], which was based on a slightly different analytical framework. But regardless of which projected return we use, the prospective returns from US equities provide an extremely modest risk premium over the 5.14% yield available on 20-year US treasury bonds. An expected equity risk premium of just 1.06% (= 6.2% - 5.14%) implies that there is about a 40% chance that equities will do no better than bonds over the 20-year time frame.

A lower equity market would restore the equity risk premium

One possibility is that the US equity market could experience a downwards correction in the next few years that re-establishes a healthy equity risk premium. In theory, this could be quite severe. In order to promise a 3% risk premium over a 5.14% US treasury bond yield, US equities would have to be priced on an earnings yield of 6.34% (calculated from 3-year trailing earnings), which implies the need for about a -30% downward correction from current levels.

Which companies are most vulnerable to a downward correction due to high interest rates?

In the near term, the companies whose share prices are most affected by rises in interest rates often seem to be those companies whose shares are regarded as “yield plays”, held by investors attracted by a reasonably high and dependable dividend yield. Share prices in such companies often fall immediately in response to higher interest rates.

At one level, this is easy to understand. Such shares represent closer substitutes for bonds than shares in more speculative companies like Tesla, so from this perspective it makes a lot of sense for the share prices of the “yield plays” to move in lockstep with bonds, while the share price of Tesla can dance to its own beat.

However, there is also a good theoretical reason for Tesla’s share price to be sensitive to movements in interest rates:

In theory, the shares in a company can be valued as the discounted value of all future cashflows that the company is expected to distribute to shareholders, with the discount rate being set at a premium over bond yields that is appropriate for the risk characteristics of the company.

The sensitivity of the valuation of a future cashflow to movements in interest rates will depend on how far it is into the future. If you are valuing a dividend that a company will pay you next month, then the present value of that dividend would drop by less than 0.1% in response to a 1% increase in interest rates, but if you’re valuing the dividends that a company might pay you 100 years into the future, then a 1% rise in interest rates should in theory lead to a 60% decline in the present value of those future dividends.

Theory says growth stocks should be sensitive to interest rates…

Shares in growth companies like Tesla are typically expected to distribute very little cash to shareholders over the next decade, such that almost all of the value of these companies is tied to the cash that their shareholders expect they may be able to pass on to shareholders in subsequent decades. As the value of these shares is heavily weighted to distant future cashflows, the valuation should be very sensitive to the discount rate used to value these cashflows. And in theory, this discount rate should be closely linked to bond yields.

Growth stocks often ignore this theory in near-term, but it eventually bites

Share markets often seem to ignore the relevance of interest rates to the valuation of growth companies in the short term, but reality eventually bites. For example, if I look at how Tesla’s share price has responded to movements in the price of TLT (an ETF invested in long duration US treasuries), it’s tended to move 26% in the opposite direction on a daily basis, implying a near-term conceit that higher interest rates are good for Tesla.

However, if I look at how Tesla’s share price has moved in relation to movements in TLT over quarterly time periods, it has tended to move 86% in the same direction as the price of TLT. (For both analyses, I looked at price movements over the past 5 years). The pretence that movements in interest rates aren’t relevant for growth investing is only a short-term delusion which can’t be maintained if interest rates keep moving in the same direction.

What if cashflows are sensitive to interest rates?

When I was using the discounted cashflow framework to consider how the valuation of equities should be affected by interest rates, I was implicitly assuming that the size of those future cashflows was reasonably independent of interest rates.

While this assumption is valid for many companies, it is not always the case.

Most obviously, some companies have significant debt, which will periodically be repriced to reflect current interest rates. Higher interest rates will reduce the amount of future cash that such companies are able to distribute to shareholders. This is a double-whammy for the valuation of these companies when you combine it with the fact that higher discount rates should also reduce the amount that investors will pay for every dollar of future cashflow.

But other companies can benefit from higher interest rates. For example, banks and insurers earn substantial income from investing “free money” in fixed interest markets. Banks get “free money” from transactional accounts on which they pay no interest, and insurers get “free money” by requiring their customers to pay insurance premiums a year in advance and then sometimes taking several years to settle complex claims. Many other business models (e.g. Airbnb) can also generate significant cash “float” which these companies are able to earn interest on. Such companies will generally see their profits increase in response to higher interest rates.

There can also be indirect impacts, whereby higher interest rates ultimately lead to higher returns across an industry, due to interest-rate-related increases in the cost of capital starving the industry of new capacity until returns increase. For example, in many apartment markets around the world rents have been increasing (due to demand exceeding available supply of apartments) but the number of new apartment developments has been plummeting, as higher interest rates mean that developers now need to see a significantly higher rental yields to justify new builds.

These indirect benefits of higher interest rates leading to higher returns on capital within an industry tend to be strongest in competitive industries where several companies may have an opportunity to provide capital, particularly in sectors where debt finance will often be used to fund capital spending (such as real estate). It is also likely to play out more quickly in sub-sectors where growing demand means that there is a continual need for new capital (such as apartments in many regions). For sub-sectors where demand is declining (such as office properties and retail properties in many regions) it could be a long time before an interest-rate-induced drop in new capital spending leads to a significant increase in returns on existing capital.

Higher interest rates can also lead to higher returns in regulated industries, such as electric utilities, where regulators often place a cap on the return that companies can earn, as the calculation of this return cap is often directly linked to interest rates.

However, for many of the most highly valued listed companies (e.g. Apple, Microsoft, Amazon, Alphabet, Nvidia, Tesla, Meta), I see little prospect that higher interest rates will have a significant impact on the returns that they are able to achieve on invested capital. While higher interest rates have not affected the outlook for these companies, they should affect the price that investors are willing to pay for theses companies, as most of the value of these companies lies in cashflows they are expected to distribute to shareholders many decades into the future.

Nicholas Bagnall is chief investment officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios hold shares in the following companies mentioned in this article: Apple, Microsoft, Amazon, Alphabet, and Meta Platforms.