Noise or trend? Or seasonal effect?

NBR Articles, published 21 November 2023

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 21 November 2023.

At a certain level, a lot of equity analysis is about predicting whether a squiggly line on a graph will move up or down in the future. For example, a key judgement is typically how fast a company’s revenues will grow in the future.

Qualitative judgement will clearly play a big role in making this prediction. Analysts will form views on the attractiveness and competitive position of a company’s products or services, look for indications of pent-up demand, and think about factors that might affect future demand.

However, a lot of these qualitative judgements will only stand up to scrutiny if they are supported by actual sales trends. If an analyst believes that the latest iteration of a company’s products will be attractive for customers, but the evidence then shows that they’re not selling very well, the analyst should probably revise their initial view!

For this reason, sensible interpretation of recent trends in a company’s sales (and costs) is an important part of investment analysis. However, there can be challenges to identifying trends in a company’s sales or costs. Sales trends can often be “noisy” (fluctuating from one calendar quarter to the next), and seasonal patterns can also make it difficult to interpret sales trends. In this column I’ll discuss some of the ways that analysts and investors can try to disentangle underlying trends from “noise” or seasonal patterns.

Seasonality

Seasonality is very common in business - many things sell more strongly at certain times of the year than at others. To use an obvious example, gift shops may do a roaring trade over the month before Christmas, but only get a trickle of customers during the rest of the year.

Although this example is extreme, most businesses experience some form of seasonality. Even businesses that charge regular subscription fees to customers - and therefore have very steady revenues from one month to the next – will often see seasonal patterns in the timing of when customers sign up to or discontinue their subscriptions.

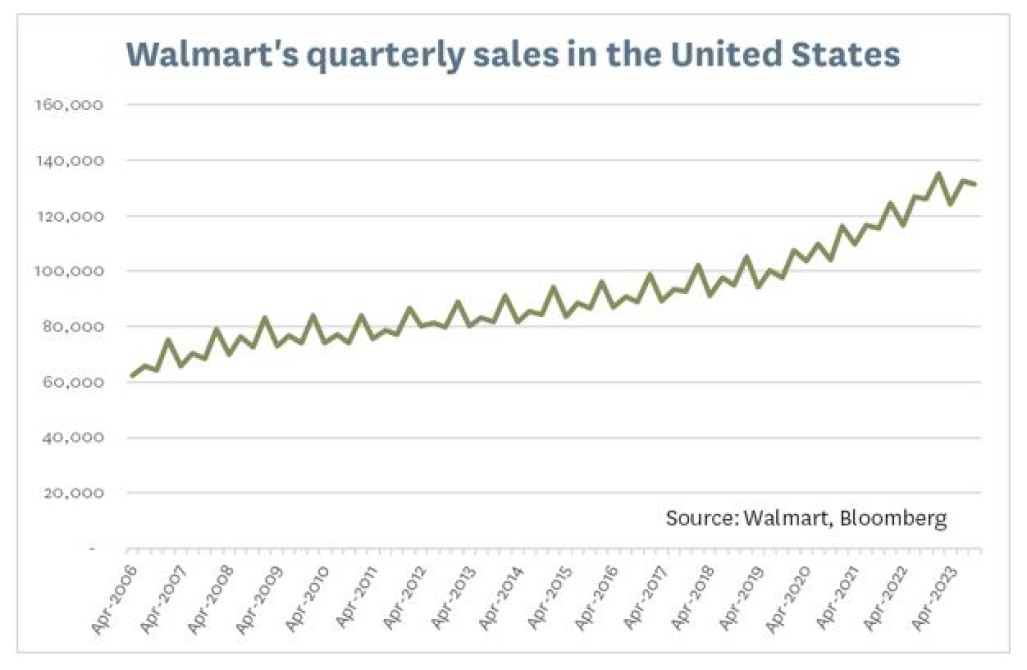

As an example of seasonality in sales revenue, consider the following graph showing Walmart’s quarterly sales in the United States (including both Walmart US and Sam’s Club). The graph is clearly zig-zaggy, with a peak in sales in the January quarter of each year (which includes the Christmas period) and a smaller peak in the July quarter of each year (corresponding to the start of the northern hemisphere summer). Troughs are evident in the April and October quarters.

How should investors evaluate trends in Walmart’s quarterly sales, given the clear seasonality? Clearly it would make little sense to simply compare each quarter to the immediately preceding quarter, as this comparison would be dominated by seasonal effects.

The most common approach that people take to interpreting data with seasonal patterns is to simply look at the change in comparison to the same period of the previous year. This generally works, because the same quarter of the previous year will have been subject to the same seasonal influences as the quarter that you’re looking at.

However, one problem with these year-ago comparisons is that they will be just as affected by conditions in the quarter-from-the-previous-year as they will be by the quarter that you’re actually interested in. Annual changes don’t distinguish the “old news” of a pick-up in underlying demand that occurred (say) 10 months ago from the “new news” of a surge in demand in the current quarter.

To identify the “new news” in a quarterly financial result, you need some way of comparing the most recent quarter’s trading with the quarter that immediately preceded it. To do this, you obviously need to try to adjust each quarter’s sales to take out the seasonal effects.

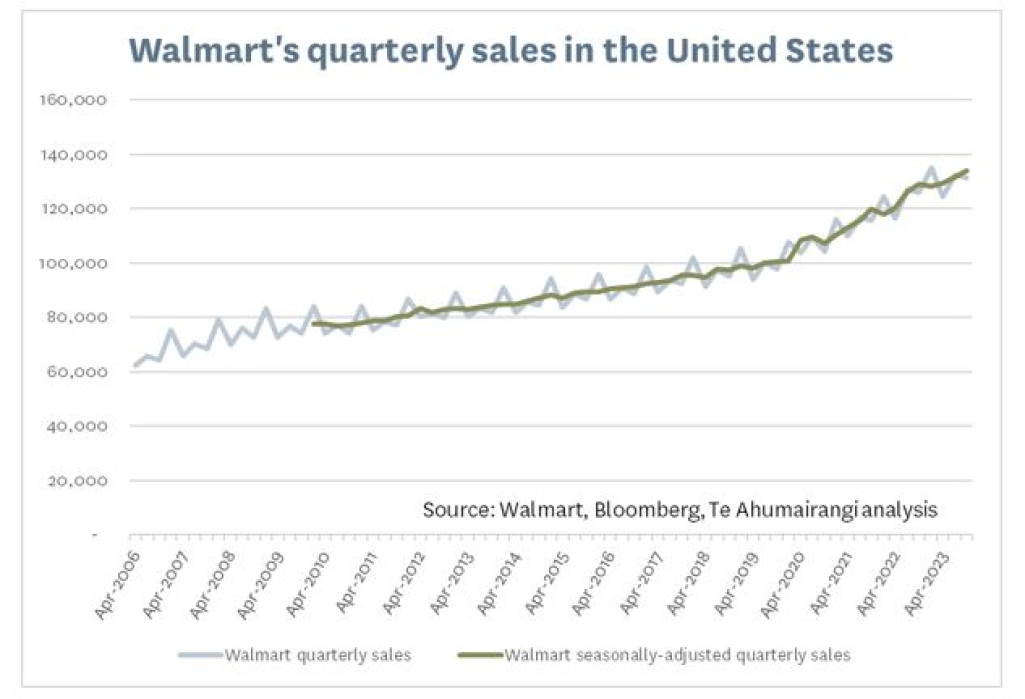

In the graph below, I “seasonally adjust” Walmart’s quarterly sales numbers by adjusting them for the seasonal pattern that was apparent in the 4 years prior to each observation (although I placed a greater weight on the most recent year). I do this by measuring the extent to which sales in each quarter vary from average quarterly sales in the year that is centred around that quarter. From this, we can define the seasonal effect for each quarter of the year as being the extent to which sales tend to be higher or lower than this centred moving average.

This seasonal adjustment removes the zig-zaggy pattern apparent in the raw data, and therefore makes it easier to compare each quarter with the quarter that immediately precedes it.

It is interesting to note that when we seasonally adjust Walmart’s US sales numbers in this way, the October 2023 quarter (the last observation on the graph) looked to have been quite a strong quarter, up 1.7% on the July 2023 quarter in seasonally adjusted terms.

This observation is interesting in light of the share market’s alarmed reaction to Walmart’s quarterly financial results, released last week. Walmart’s shares fell -8.1% on the day of the earnings release. While some part of the market’s reaction was a response to other aspects of the result, including Walmart’s comments about a deflationary outlook, it does seem that a large part of the market’s disappointment related to slowing annual growth rates in Walmart’s US retail businesses.

The analysis shown in the graph above suggests that the slower annual growth rate in Walmart’s October 2023 quarter was a reflection of unusually strong US sales in the October 2022 quarter, rather than weak sales in the October 2023 quarter. If fact, our seasonally-adjusted numbers suggest that after growing in the October 2022 quarter, Walmart’s US sales had been fairly weak in seasonally-adjusted terms in the January 2023 quarter and have picked up over the subsequent 3 quarters. The fact that the January 2023 quarter was quite weak implies a likelihood that the calculated annual rate of sales growth should improve in the upcoming January 2024 quarter.

This analysis suggests that the -8.1% decline in Walmart’s share price was an over-reaction to the “new news” embedded in their October 2023 financial results. However, this does not necessarily imply that Walmart is now cheap, as it out-performed the market in the lead-up to the result release, and the market values it on significantly higher earnings multiples than competing supermarket companies.

Trending or reverting?

A key question when we see an unexpected strong or weak sales result (after adjusting for seasonal effects) is whether the surprise is indicative of a change in trend or whether it is just a one-off change that might reverse out in the following quarter.

An analytical framework can be important in evaluating this question, as without it some sell-side analysts seem to have a strong tendency to always interpret new information in the same way. The more excitable analysts have a tendency to always assume that an unexpected sales result represents a change in trend while some “ostriches” bury their heads in the sand and look for reasons to interpret any sales surprise as being due to one-off factors. Confirmation bias can also play a role, with some analysts quickly embracing any data point that adds weight to their thesis, while finding one-off factors to explain away any outcome that is contrary to their prior viewpoint.

One way of evaluating whether a surprise in a company’s sales is likely to be indicative of a change in trend or just noise is to look at the historical pattern in a company’s seasonally-adjusted sales. (Specifically, we can look at the serial correlation of quarterly changes in seasonally-adjusted sales: positive serial correlation indicates trending, whereas negative serial correlation indicates noise.)

Using the Walmart example above, we find that there is an element of “noise” which means that above-trend increases in seasonally-adjusted sales tend to be followed (on average) by slightly below-trend sales increases over the following two quarters. However, the data shows some longer-term trending, with stronger-than-average quarterly sales results pointing to stronger-than-average quarterly sales increases between 3 and 6 quarters into the future. Overall, the historical data indicates that (all else being equal) if Walmart announces 1% stronger sales in the current quarter, we should probably lift our expectation of sales two years into the future by somewhere between 1.0% and 1.2%.

This short-term reversion combined with modest trending over the medium term is pretty typical for large mature businesses, but different businesses can have a different tendency to trend or revert. Working out what sort of business you’re looking at is important, as it will inform how strongly you should react to a sales surprise.

For many companies, we won’t have enough meaningful historical data to make a good inference about whether sales will tend to keep trending in the same direction, or whether they’re more likely to bounce back in the opposite direction. It is therefore important to supplement or replace any statistical analysis with the insight that we can get some rules of thumb that help us determine whether a sales surprise is indicative of a change in trend or just noise. Some of the rules of thumb I find useful are:

- Sales surprises are more likely to be noise for companies with lumpy sales (e.g. construction companies, to use an extreme example).

- Sales surprises are most likely to represent change in trends for companies that get most of their revenue from subscriptions or other regularly recurring revenue from the same customers. If a company gains a new subscriber half-way through the quarter, then they’ll get one and a half months of revenue from the subscriber in that quarter, followed by 3 months of revenue in the next quarter, thereby continuing the upward trend in revenues.

- Sales increases due to market share gains often persist in the same direction for much longer than changes due to the economic cycle. For example, consider the fashion industry, where aggregate sales can rise and fall from one year to the next, but individual retailers can steadily gain (or lose) market share over the course of a decade.

- Sales have a greater tendency to trend for rapidly growing businesses than for businesses that are growing more in line with GDP. For example, with the cloud services businesses of Amazon’s AWS and Microsoft’s Azure, there is a strong tendency for growth in one quarter to be followed by similar growth in the following quarter.

- Company management will often call out one-off factors that they believe have affected the results, and it is important to consider these factors. However, this should not be done blindly, as company management are far more likely to look for excuses when they deliver poor results than to highlight any tailwinds that helped them deliver better-than-expected results.

Separating the trend from the noise in company results involves both art and science. It is important to think carefully about what the results are really telling you and avoid jumping to conclusions too early.

Nicholas Bagnall is Chief Investment Officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios hold shares in Walmart, which is discussed in this article.