What drives margins?

NBR Articles, published 12 September 2023

This article, by Te Ahumairangi Chief Investment Officer Nicholas Bagnall,

originally appeared in the NBR on 12 September 2023.

When we think about how a company’s profits might change over the next decade or more, it is natural to think mainly about whether the company is likely to experience a significant change in its levels of sales, and to assume that profitability will trend in the same direction.

Revenue (= sales) growth is clearly the principal driver for most of the companies that top the charts for growth in profits. After all, a company that’s starting from a point of reasonable profitability has little chance of achieving ten-fold growth in profits unless its revenues grow at least five-fold.

However, only a small percentage of companies will grow this fast. Over extended periods of time, most companies will grow their revenues at relatively modest single-digit rates. When we look back in ten years’ time at the financial performance of the companies that are listed today and already have over a billion dollars of annual sales, I’d expect that we’ll see that with hindsight, the vast majority of them will have achieved organic sales growth (i.e. growth before the effect of acquisitions or divestments) of somewhere between 0% and 10% per annum.

However, when we look back in 10 years at the investment returns that these modest growers have achieved, I would anticipate that we’ll see far greater dispersion than might be implied by the relatively tight clustering of their revenue growth rates. A lot of this dispersion will be due to changes in how much profit companies make for every dollar of sales.

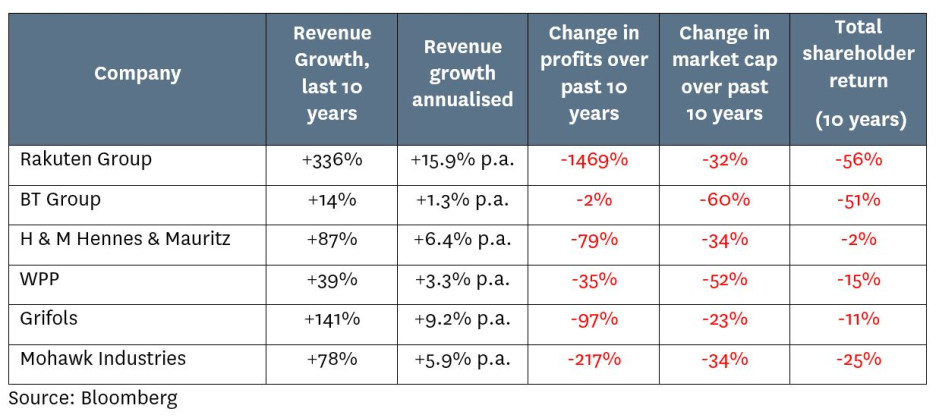

For example, compare this group of companies that have achieved modest-to-significant revenue growth over the past decade but have nonetheless experienced a decline in market capitalisation over this period and have delivered poor shareholder returns…

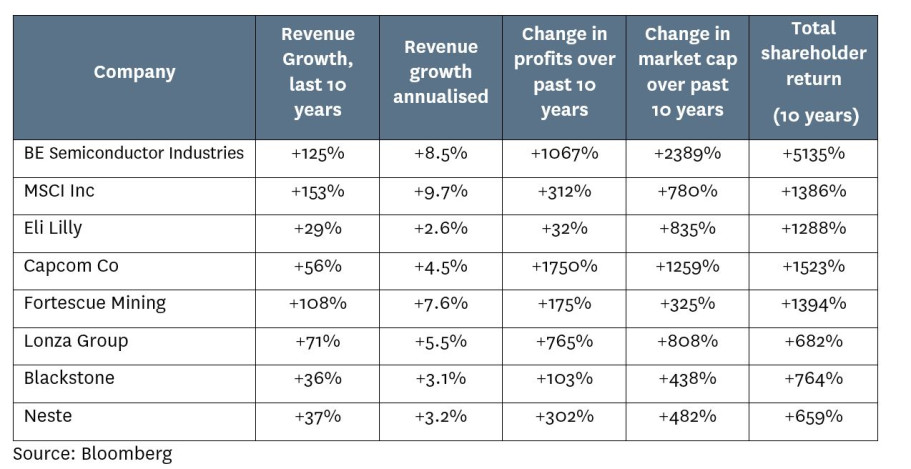

… to the following of companies that have also experienced modest revenue growth but have delivered fantastic shareholder returns on the back of strong increases in market capitalisation…

From the first table, it should be clear that growth in revenues is no guarantee of good shareholder returns, and from the second table, it is equally clear that strong growth in market capitalisation can often be achieved by companies that only achieve modest revenue growth.

If you look closely at these tables, you can see that changes in market capitalisation are often more closely related to changes in a company’s profits than changes in its revenues*.

The tables also reveal that profit growth oftens diverges significantly from revenue growth. Divergence between a company’s revenue growth and its profit growth will typically be mainly due to changes in its operating margins. If a company’s operating profits grow faster than its revenues, then by definition, its operating margin (= operating profit divided by revenues) must have increased.

[ * Note that in the second table above, Eli Lilly is an exception to the rule of changes in market capitalisation having had a close relationship to changes in profitability. In Eli Lilly’s case, profits have only risen modestly over the past 10 years, but its market capitalisation has shot up on expectations that its diabetes drug Mounjaro will be approved as a cure for obesity and could achieve hitherto-unprecedented levels of pharmaceutical sales and profit by 2030.]

Predicting changes in Operating Margins

These examples indicate that it would be extremely useful if an investor could predict how operating margins are likely to change over the next decade. But predicting changes in margins often seems to be more difficult than predicting growth in revenues. This is probably the reason many sell side analysts seem to routinely assume that future margins will be close to where they are today.

Despite the difficulties, the remainder of this column is going to discuss some things we should look at when thinking about the prospect of a change in operating margins.

Reversion

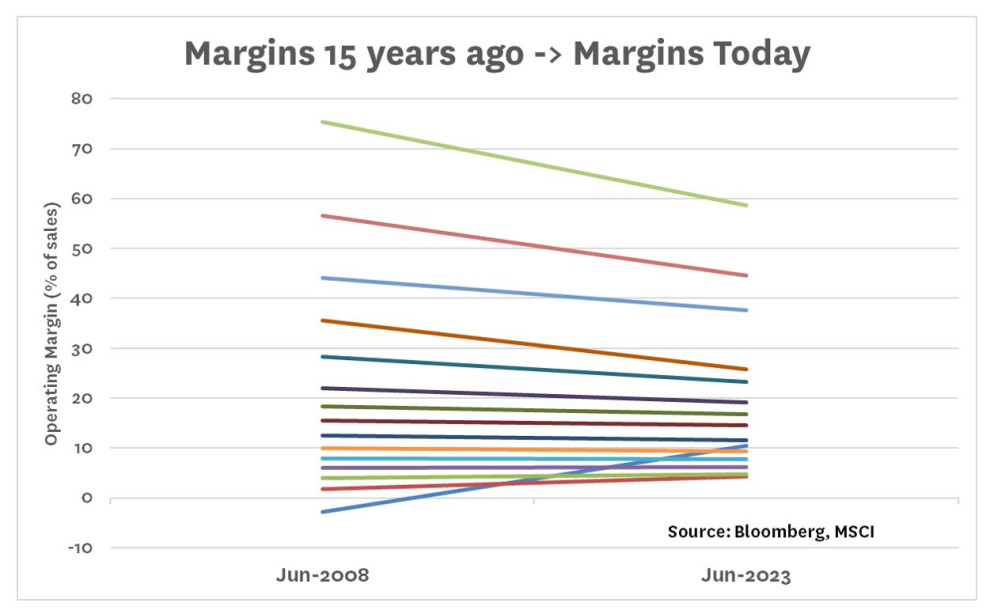

In the graph below, I’ve looked at all the companies included in the MSCI World index in 2008 that are still listed today, and sorted them into buckets based on the trailing operating margins they had achieved over the year up to 30 June 2008. For each of these companies, I’ve then looked at the operating margins that they’re achieving today, and calculated how the average operating margin has changed for each bucket of companies.

If you examine this graph, you can see that while high-margin companies have tended to remain high-margin companies, and low-margin companies have tended to remain low-margin companies, there has also been an element of reversion. Generally speaking, the higher a company’s operating margin was 15 years ago, the more it has declined over the subsequent 15 years, and the lower a company’s margin had been, the more likely it is to have subsequently increased.

This suggests that we need to be aware that neither good times nor bad times always last forever. If a company is achieving particularly high operating margins right now, the balance of risks is that something will cause those margins to narrow in the future, and if it’s experiencing particularly low margins right now, the balance of risks is that something will improve in the future.

Operating Leverage

The driver of margins that is perhaps most well-understood by financial modellers is operating leverage. Most businesses have a combination of some costs that are inherently linked to revenues (for example, the costs of buying goods for resale) and other costs that are more fixed in nature and won’t directly increase in the short term if the business gains more revenue. For example, most businesses pay fixed monthly rentals for their premises, so if sales increase, the rental expense will decrease as a percentage of sales, such that operating margins will increase.

Operating leverage tends to be an extremely important driver of operating margins in the short term. For businesses that face no direct competition, operating leverage can sometimes drive margins for several years, with operating margins increasing year after year as revenues continue to outpace fixed costs.

However, it is easy to over-estimate the power of operating leverage to drive up margins over the longer term. As companies grow and become more profitable, a number of forces can conspire to push up their supposedly “fixed” costs. As they get larger, businesses will come under pressure to develop new product offerings, open in more locations, strengthen their compliance systems, pay executives more, and so on. This often means that businesses which theoretically had a large element of “fixed” costs find that in reality these costs grow almost as fast as revenues.

Further, after a long period of super-normal growth, companies tend to develop a “growth culture” whereby employing new staff, starting new projects, and adding new items of cost is considered “normal business”, and as a result, a company’s expenses can build super-tanker momentum which means that costs will continue to grow even if the company’s top line slows down to more normal rates of growth.

We’ve seen this over the past year with many of the mega-cap tech companies, which are experiencing slower revenue growth than they were historically accustomed. Over the past year, Microsoft, Alphabet, and Meta have all experienced declines in operating margins despite continued (but slowing) revenue growth. Each of these companies disclosed cost-cutting measures in the second half of 2022, but the impact of these measures has so far been insufficient to turn around the momentum in their corporate cost machines.

Competitive conditions

While an accountant or financial modeller used to looking at changes in profitability over two or three years might think of operating leverage as the most important driver of changes in margins, a micro-economist would argue that margins will ultimately be determined by a company’s competitive environment.

Perhaps reflecting a bias inherited from having studied economics myself, I also share the view that changes in the competitive environment will ultimately be the biggest driver of changes in a company’s profitability. Operating leverage often helps us to understand whether a company’s margins will increase or decrease from one year to the next, but if we’re thinking about how a company’s margins / profitability will change from one decade to the next, I believe it is critical that we think about how the competitive environment is likely to change.

This “economists’ view” of changes in the competitive environment will often conflict with the “accountants’ view” of continued operating leverage, for the simple reason that an economic perspective will observe that growing revenues and high returns/margins tend to attract more competition, whereas poor returns/margins and moribund growth tend to lead to rationalisation, under-investment, and reductions in capacity.

This cycle is most obvious in commodity-like businesses. If the pricing of a particular commodity (say, iron ore) is strong, high margins (and therefore returns) will encourage many companies to invest in producing more of that commodity, and as production ramps up, it is likely that prices and margins will ultimately decline.

However, this cycle of high margins & returns attracting increased competition (which ultimately depresses margins & returns) will often take a lot longer to play out for companies that are achieving high returns from a unique product offering. This will particularly be the case where there are significant barriers to competitive entry or where customers may find it particularly inconvenient to switch from one supplier to another.

These barriers to competitive entry seem most persistent when they are due to an unregulated network effect, where there are rational reasons for customers to prefer to use the same product as everyone else.

For example, it would be hard to make a success of launching a new social network in 2023, as people generally go on social networks to interact with others, and hence are unlikely to be interested in a new social network that doesn’t already have a large number of users.

Another example has been Microsoft’s Office suite (Word, Excel, etc). For at least two decades there have been significantly cheaper alternatives to the Microsoft Office suite which have reasonable compatibility with Microsoft Office, but these alternatives have achieved very little traction with businesses, because it is most important to businesses that employees are able to use spreadsheets and word processing software that they familiar with, that the software they use is fully compatible with other software used by the business, and that they can easily exchange files with other businesses.

However, such network effects will sometimes be broken by regulation. For example, the profitability of the telecommunications industry plummeted globally after regulators forced telecommunication operators to inter-connect at zero cost and to allow users to take their phone number with them when they switched networks.

Barriers to entry from technology leadership seem to be more difficult to sustain. While I can think of several examples of companies that have enjoyed strong profitability for periods of up to a decade due to technological leadership, I struggle to think of many examples of companies that have kept ahead of their competitors and maintained high margins for as long as two decades simply by maintaining technological leadership.

This point is pertinent to Nvidia, which has seen its market capitalisation rise by US$800 billion this year based on its technological leadership in designing chips that are optimised for training AI models. In the short term, operating leverage has been the best explanatory model for Nvidia’s operating margins, which rose from 7.4% in the July 2022 quarter to 50.3% in the July 2023 quarter on the back of a doubling in revenues. But at the same time, we’re seeing a huge step up in plans by other companies to develop chips to compete with Nvidia’s AI-focussed GPUs. Given this increasing competitive activity and the patchy historical record for companies maintaining leadership based on technology alone, I suspect that the 50% margins that Nvidia’s now achieving from the AI boom are more likely to revert downwards over the next couple of decades, even though the volume of semiconductors that it sells will most likely continue to grow rapidly. Nvidia stands to make a lot of money over the next few years, but with the sharemarket valuing it at over 100 times trailing earnings, we need to have more confidence that it can maintain its leadership than we might get from studying past cases of technological leadership.

Understanding what a “normal margin” should be for a particular industry

In understanding the operating margins that a company might achieve in the future, it is often useful to understand how the economic characteristics of the company compare to those of other companies and industries, and to draw parallels that help us understand what margins the company might be able to sustain in the future.

Different industries can be intrinsically high or low margin, depending on many factors, including:

- the price sensitivity of customers (do they shop around?);

- industry structure (few or many competitors?);

- the cost of manufacture in relation to the value proposition for customers (it is generally easier to make high margins from products that deliver a lot of value but cost very little to produce!);

- market power relative to other participants in the value chain (sometimes it is the company’s supplier or re-seller that secures the lion’s share of the profit); and

- demand vs capacity (margins will tend to be high when an industry is struggling to meet demand).

Margins can also vary in different ways across different participants in an industry. In some industries, all competitors achieve similar margins, but in other industries with a large fixed cost element (e.g. software, media, and telecommunications) there tends to be a winner-takes-all dynamic where the company with the largest market share makes most of the profits.

This history of margins in a particular industry in different geographies around the world can be a good indication of where margins are likely to settle in the future.

To my mind, bulls on Tesla represent a good example of people focussing on the sales potential of a product without fully understanding what drives margins. The history of the automotive industry clearly shows that it has not been a high-margin industry, particularly when you consider the mass market segment (rather than the aspirational luxury part of the market where Tesla began).

The reasons for this should be easy to understand. Cars are an expensive outlay for most customers, so they tend to shop around and pay a lot of attention to price. Manufacturing costs are high relative to the value proposition that cars offer to most consumers, so there is less opportunity for high margins than is the case with (say) a bottle of water or a life-saving pharmaceutical that costs a few cents to manufacture.

And the automotive industry is also highly competitive, with numerous participants. While there was a period when Tesla largely had the Battery Electric Vehicle (BEV) market to itself, this clearly is no longer the case, and most automotive manufacturers are planning to significantly increase production of BEVs.

If you conclude (as I do) that Tesla’s long-term average operating margins will most likely be no more than 10%, then it is almost impossible to consider Tesla a good long-term investment almost regardless of what share of the global automotive market you think it will ultimately achieve.

Nicholas Bagnall is chief investment officer of Te Ahumairangi Investment Management

Disclaimer: This article is for informational purposes only and is not, nor should be construed as, investment advice for any person. The writer is a director and shareholder of Te Ahumairangi Investment Management Limited, and an investor in the Te Ahumairangi Global Equity Fund. Te Ahumairangi manages client portfolios (including the Te Ahumairangi Global Equity Fund) that invest in global equity markets. These portfolios hold shares in the following companies mentioned in this article: Microsoft, Alphabet, and Meta Platforms.